Unanimously, I can already hear the entire personal finance community scream “NO! Absolutely not!”

But what’s interesting is that three of the most-often quoted people in retirement planning seemed to think so: Cooley, Hubbard, and Walz.

Just in case you’re not familiar with the names of those personal finance rock stars, they are the three authors who penned the historically important, ultra-popular “Trinity Study”.

Yes, the same Trinity Study that validated Bill Bengen’s 4 percent rule and made it one of the most wildly popular tools in retirement planning to date!

So then, if the authors validated the 4 percent rule, what is this business about a 7 percent safe withdrawal rate?

There’s a small caveat, of course …

Let me explain it further.

A Gold Nugget in the Trinity Study

While doing some research for my next ebook (which will be heavily on the subject of safe withdrawal rates), I read the updated version of the Trinity Study (April 2011, Journal of Financial Planning), which is actually entitled “Portfolio Success Rates: Where to Draw the Line”, and noticed something that most people never talk about (or perhaps overlook):

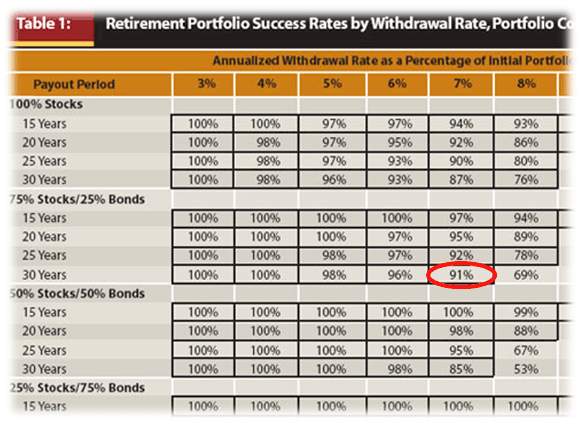

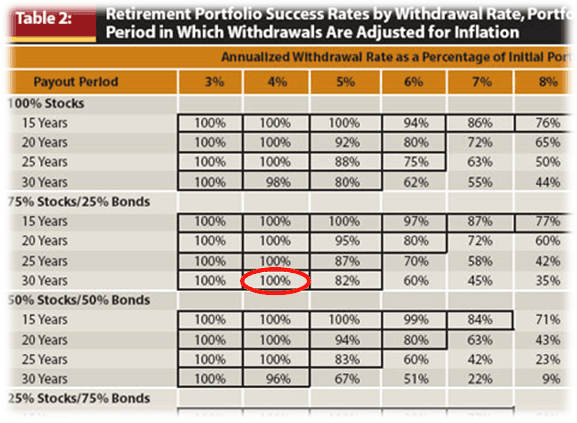

The Trinity Study actually provides safe withdrawal rates that are both inflation adjusted and non-inflation adjusted returns.

While that might not seem like a big deal, it quickly becomes very interesting when you see that the authors conclude that a non-inflation adjusted safe withdrawal rate of 7.0% for a portfolio of 75/25 stocks and bonds has a 91% chance for success of lasting 30 years or more!

When you compare that to the more commonly quoted inflation adjusted 4.0% safe withdrawal rate (which has a 100% chance for success with a 75/25 stocks and bonds portfolio), it poses some interesting prospects.

Inflation Adjusted vs Non-Inflation Adjusted

Let’s think about what non-inflation adjusting means for a minute.

Especially if you’re late to saving for retirement or struggling to get there, this tidbit of information could make reaching your goal a whole lot easier.

How much easier? Say you were hoping to retire and withdraw $5,000 per month (or $60,000 per year). Under the traditional Bill Bengen 4% rule, you’d need a nest egg of $60,000 / 0.04 = $1,500,000. But that would also provide you with inflation adjusted returns. In other words, if we assume 3% inflation, that would be $60,000 this year, $61,800 the next year, $63,654 the year after, and so on.

However, if you didn’t need to adjust for inflation and you used a rate of 7.0% instead, then you would only need a nest egg of $60,000 / 0.07 = $857,143. That’s a difference of 43% less! That’s HUGE!

What This Information Means for Us

Am I declaring that everyone should adopt a 7.0% safe withdrawal rate?

Of course not! (It was just a clever blog post headline.)

The real value in this information is that it provides us with a range (or a “tolerance” as we call it in engineering) rather than a single target.

Going back to my previous example using the 4 percent rule, someone might believe that $1.5 million was the end-all-be-all target that they needed to hit in order to achieve financial freedom.

But in reality, if we are willing to compromise on what, when, and how we adjust for inflation, a nest egg ranging from anywhere between $857K and $1.5M may get us to where we need to be!

Or alternatively, we could also increase our chances of making our money last well beyond 30 years if we’d like a higher level of confidence that we won’t deplete our nest egg.

There are many useful applications!

But Don’t You Have to Adjust for Inflation?

Of course you’re probably saying to yourself “Wait! You HAVE to adjust for inflation every year. Otherwise, you’ll lose the purchasing power of your money!”

And that may be true. But let’s stop to consider a few scenarios.

Remember that inflation is an aggregate term, meaning that it assumes that the price of everything went up.

But does it?

While your household goods, restaurant meals, and other discretionary purchases increased with time, some things probably won’t. For example: Your mortgage payment. If you’ve got a fixed interest rate, then your principal and interest rates will stay the same for 30 years!

Or consider your car payment. Once it’s paid off, you don’t to necessary buy another car right away or even buy one that is just as expensive. Like all your expenses, by shopping around and getting multiple quotes first, you usually get the same or sometimes a better price year to year.

How many times have you not received a raise at work, and were fine without it? Lot’s of people have this problem for one, two, or sometimes many years in a row. And they get along just fine without one. In fact, from personal experience I can tell you that for many occupations, once you reach a certain wage threshold, you stop getting raises altogether.

In our example above, the difference between the first year and second year of $61,800 was only $1,800. That works out to $150 per month. Are you really going to miss $150? More than likely you’ll find a way to adjust. This was this was exactly a phenomenon that Robert and Robin Charlton had experienced in their book “How to Retire Early”. They were able to go multiple years without needing to adjust for inflation.

Do you really need exactly the same amount of money year over year? Perhaps your needs change over time and can adapt as your life gets older. For example, maybe you don’t travel as much or have the same sort of expenses any more. For example, maybe you finally pay off your mortgage and don’t need to cover that expense any more.

One thing that everyone always forgets about: Social Security! Remember that you’ve been paying into it all this time and by all accounts are still entitled to a subsidy. According to their website, after 2034, you can expect to receive at least 75% of your benefit by the time you retire. So if you’re worried that after 10 or 20 years your purchasing power will dwindle down to far, your Social Security payments may give you that extra boost you need.

Finally, remember too that inflation adjusting doesn’t have to be an “all or nothing” application. For instance, you could go 2-3 years without making an adjustment before you raise your income amount. Or maybe you raise your income level by 1 or 2% instead of the often quoted 3%.

Conclusions

Again, while I’m not suggesting that a 7.0% safe withdrawal rate is something you should adopt, I do believe there are several useful applications we can take away from reviewing this data:

- If you’re struggling to save for retirement or late to the game, you could use the non-inflation adjusted strategy to generate the income you desire from a lower nest egg.

- If you have any doubts about the validity of the 4.0% rule, then you could always hold off on making inflation adjustments to gain more certainty that your portfolio will last 30 years or longer.

- If you need your money to last longer than 30 years (say 50 or more if you plan to retire early) and plan to withdraw 4.0%, again, you could hold back on making inflation adjustments. This would likely boost your chances for success since you’d be well below the 7.0% rate.

Readers – Have you ever considered NOT adjusting for inflation as a potential strategy for prolonging the life of your nest egg? What do you think about this detail from the updated Trinity Study, and could it be useful in your personal financial freedom plan?

Featured image courtesy of Flickr | Heather aka Molly

I need to take a deeper look into the Trinity Study, Recently I’ve been re-evaluating some of the “written in stone” rules of personal finance, and this is a big one. It’s crazy how widely accepted the 4% rule is and how virtually everyone subscribes to it, or falls on the other side saying a 2% – 3% withdrawal rate is the only way to be safe. I can easily see moving up to a 6% and possibly a 7% withdrawal rate and feeling comfortable. This is also really good information to put out for people struggling to build a retirement fund, which is easily well over 75% of the U.S. population.

It’s really amazing how the more you read about SWR’s, the more you realize that there are a multitude of ways to manipulate them. And this is a good thing because it means we can accomplish more with fewer assets. For people who haven’t saved like they were supposed to, there is hope!

Hi DJ,

This is a great post and raises some interesting points. I left Corporate America three years ago to focus on building my own small eCommerce business. I didn’t “retire” and so I’ve been living off of my emergency fund.

What I’ve found is that you can spend less if you really want to. Your clothing needs change, you don’t tend to drive as much, I spend less on makeup because I don’t wear it as much…and the list goes on.

I had a $1.2 million target as my desired “nest egg” (excluding assets like my house) before starting to withdraw from my retirement savings. If things don’t fly with my business, I’ll miss that mark by a lot.

But…

I have altered my retirement strategy to this:

– Begin to withdraw at a rate of 2% at 59 1/2.

– Make up the difference between what that provides with an earned income or draws on my business until I reach full retirement age, or better until 70.

– This lets my SS benefit grow to the maximum allowed.

– Over the years of the 2% withdrawal rate, increase it as needed (and reasonable) up to 4%.

This is my current plan. I’m a couple years away from implementing it so it may change between now and then depending in part on how well my business and assets do in the meantime.

Thanks for making us think outside the box!

You bring up a great strategy; one that people often overlook because of the word “retirement”: You can still use your talents to earn money! Just because you might have achieved financial freedom or are living off of your assets doesn’t mean you can’t start a side business or work part time. But by doing so, you can significantly supplement your need for those assets, and that just increases the potential that they will last longer over time.

A SWR of 2% is about as ultra-safe as it goes. I haven’t read a legitimate study yet where 3% was the cut off for near certainty.

Very interesting study you found here. I think the main reason the 4% rule is so popular is because of the 100% chance of it being available after 30 years and in this day and age when life expectancy continues to rise it seems logical for many people. Withdrawing 7% per year without any income coming in may quickly deplete your savings but like you said you are not increasing your withdrawal rate as inflation is not taken into account.

I think the main draw of the 4 percent rule is its simplicity. Nearly anyone can use and understand it. For those who profit trying to make personal finance seem a lot harder than it really is, it’s a total nightmare!

When it comes to costs, I know you’ve written here and in your second ebook about LOWERING your bills (auto insurance, cable, etc). Maybe not all of your costs are destined to increase at the rate of inflation, even as the value of the money decreases.

Plus, just because you’ve retired doesn’t mean you’re relying on that static numbered nest egg. Pension and annuity payments last a lifetime, as do dividends from dividend stocks if you never sell and you’ve bought high quality companies. Plus, it’s not impossible to go out and make more active income! Even an elderly person can find a decent work at home job. I did before and am looking for a new one now!

As a side note, 75 cents on the dollar for Social Security payouts? Criminal. I’d rather just have my money refunded to me now, cease paying the Social Security tax, and just not actually get payouts in the future.

I think I went off track there. Amazing find with the Trinity Study! A ~7% rule? Maybe your name should be on the updated version?

Sincerely,

ARB–Angry Retail Banker

I agree! People often forget that the 4 percent rule is just for planning. In reality, if you’re flexible with your spending or are willing to actively find opportunities to make a little money on the side here and there, then you’ll be more than okay!

On Social Security, I think we may see that system change morph over the years. It wouldn’t surprise me if 50 years from now we all have some sort of government pension program similar to a 401k but mandatory by Federal law.

Interesting post, but this is no free lunch. Logically, you cannot expect a 75% higher spending withdrawal (7% is 75% more than 4%) to have a small impact on retirement finances. Unless you are confident of dying younger than an average lifespan so you want to enjoy the early retirement years, this strategy us risky. Inflation is like a slow cancer, you won’t notice it in early stages until one day if you don’t treat it, it will kill you.

No, you’re right there is no such thing as a free lunch. But for someone who is age 45 and has almost nothing saved for retirement, this sort of a thing could be useful. Plus, you have to remember that Social Security eventually kicks in. That extra income will solve the offset in the inflation difference.

Your calculations work if In summary – the future is like the past ( !!??!!) and if you are lucky (!!!???!!!)

these are big IFs

Why not? The market is cyclical. Look at any 30 year stretch and you will see.