That’s a really good question.

I’m sure for a lot of people (myself included) that the money you have in your 401k account is probably the largest percentage of your wealth you have saved up – anywhere! Even if you’ve got nothing more than the average 401k balance of $81,000 as reported by Fidelity, that’s still a very serious amount of retirement savings that you want to be putting to work as hard as possible.

Unfortunately, however, that’s not always what we do. Dozens of studies have shown that simple missteps like leaving your funds in accounts with too high of fees and low performance can result in hundreds of thousands of dollars in returns lost over the years. And those losses would be due to nothing more than pure negligence.

So in the post, I’m going to show you how to take charge. We’ll explore some of the benefits and drawbacks to a potential 401k rollover into an IRA and see where it might make sense for you and your plan for financial independence.

Really your decision making will boil down to three major areas:

1. Accessibility to Your Money:

I’m going to start off this whole discussion with accessibility first. This is because I don’t think a lot of people realize something about their 401k accounts:

- You’re employer has you on a leash when it comes to accessing your 401k.

On my other blog about retirement planning, I’ve received dozens of comments and emails about how a person would want to borrow or withdraw from their 401k account only to be denied by whatever rules the employer has in place. That means no borrowing or early access as long as their employed at that job. While you might think this is illegal or unethical, unfortunately that’s the way it is depending on the individual rules your employer has setup for your job.

In comparison, when your retirement savings are in your IRA, YOU control whether or not you can access to it. Not your employer or even a former employer.

Now you could argue that you shouldn’t go dipping into your 401k or any retirement savings really until you’re truly ready to retire. And in a perfect world that is correct.

But what about emergencies? What about the unknown? What if you want to take out early withdrawals using a 72t? Wouldn’t it be nice to know you could do it if you wanted?

For that reason alone, if I ever changed jobs and had the opportunity to do a 401k to IRA rollover, I would do it in a heartbeat!

But that’s me. If none of this is important to you, then don’t sweat it. Maybe your money can stay right where it is in the old 401k. However before you come to that conclusion, consider the next few points and see if any of these are reason enough to move your balance over.

2. What Are the Fees in Your Old Plan Like?

Fees are the next thing I’d be concerned about when evaluating your old 401k plan. Classically most 401k plans have higher fees than IRA’s because you’re paying for two things:

- Fees on the mutual funds themselves (set by the investment provider).

- Administrative fees to keep the 401k plan running.

Now compare those fees to those of a basic IRA plan.

- Depending on where you look, you can find lots of mutual funds that have incredibly cheap expenses. Just check out the Vanguard Total Stock Market Index Fund Admiral Shares (VTSAX). For a balance of $10,000 or more you qualify for an expense ratio of 0.05%. That’s only $5 for every $10,000 you invest!

- The common investor doesn’t pay administrative costs on their IRA, so that part of the issue goes away.

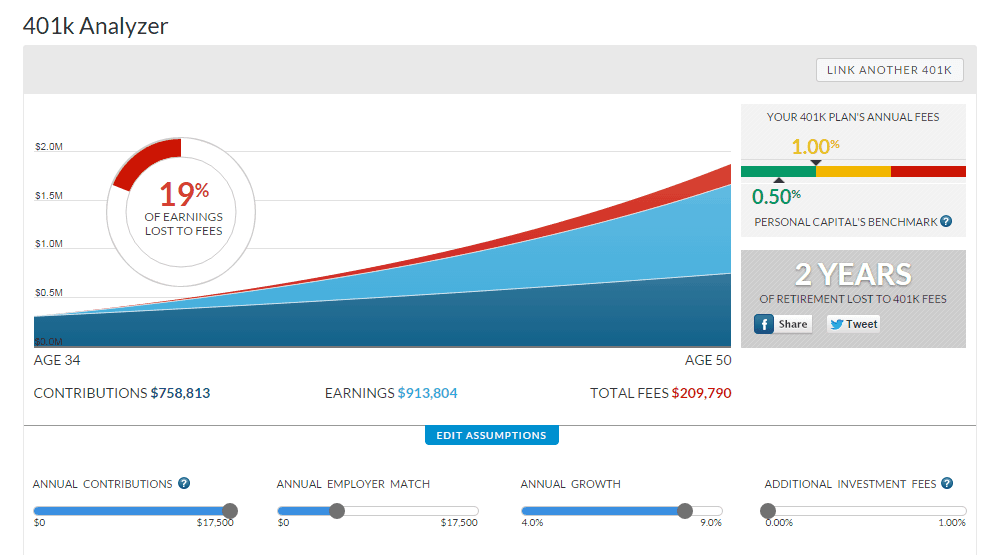

To give you an idea of the magnitude of those 401k fees over time, check out the 401k Analyzer for my own 401k using this free service from Personal Capital. Using their default variables, it looks like over the next 16 years I’m going to lose $209,790! Ouch!

I’m confident that if most people took a closer look, they’d find that the IRA fees in most situations are going to be a lot less than what you’re probably paying now in your current or old 401k.

3. How Did Your Investments Perform?

This is the last thing to consider, and I think I can sum this up for you pretty easily.

Look at your 401k plan over the past 5 or 10 years and compare it to the performance of a stock market index fund (such as the Vanguard one I mentioned above). I’m going to guess that it probably didn’t do as well as the index fund, did it?

That’s because no matter what you think you know about stocks or investing, most of us are probably better off with simple index funds for our retirement savings rather than a bunch of exotic actively managed funds in our old 401k.

Therefore, unless your 401k is somehow delivering some absolutely stellar returns, you can rest assured that your investments are probably going to do just fine in the rollover IRA emulating the average market returns.

Very Important Questions to Ask Before Making a 401k to IRA Rollover:

- What will the taxes be like? This one is huge! Basically while doing your rollover, you’ll be presented with two types of IRA’s – a Traditional or Roth. Choosing the right one will be critical. If your 401k was setup as a traditional-style account (no taxes paid now, you pay taxes when you retire), then a Traditional IRA will probably be the right direction to go. Why not the Roth IRA? Technically you could go with the Roth IRA. But because on Roth accounts you pay taxes NOW, not at retirement, you’d have to pay taxes on the entire balance. Here’s a quick approximation: If you’re in the 25% tax bracket, then for every $100,000 you have in your account you’d owe $25,000 in taxes THAT year! Ouch! So unless you have an incredibly compelling reason to go with the Roth, stick to a Traditional.

- Where should I rollover the 401k to? If you already have an IRA with someone, that’s probably a good place to start. I personally use Vanguard (no affiliate relationship) for all my IRA accounts because they are cheap and have some of the most reputable funds.

- What will it cost with the new investment broker when I roll over my old 401k? Every investment broker will have a different answer for this. But fortunately most of the larger, discount ones will likely cost virtually nothing. Again using Vanguard as an example, I was informed that the cost for a 401k rollover is free. You gotta love free!

- What is the fee from the old 401k plan provider to complete the rollover and close out the account? Don’t just consider the new investment broker. The old one may also have some fees associated with closing out the account as well. I asked this of my own 401k provider and found out it will only cost me $50.

Readers – I’d love to hear your opinions or experiences with a 401k to IRA rollover. Have any of you asked this same question or experienced any of the things we talked about above? Did anyone find that leaving their 401k balance right where it is was the right choice? I’d love to hear.

Images courtesy of FreeDigitalPhotos.net

Greg rolled his old work 401K into his SEP IRA with Vanguard. He’s no longer contributing to the SEP since he has a work 401K again, but that money is much better off there. The Edward Jones fees were ridiculous compared to Vanguard.

Actually, you can contribute to both a 401 (k) and SEP IRA, provided you follow IRS limits closely.

Say if you earned some salary and maxed out 401K with $17.5K, and earned say $20K from a gig you do on the side, you can put something like $4K in the SEP.

Best Regards,

Dividend Growth Investor

Excellent advice, but you can take it even a step further. Last year (with the help of a tax professional) I was able to max out the 401k, my Roth IRA, and contribute to a SEP IRA with my blog earnings. Not only did this small unknown strategy allow me to save above and beyond what I normally do, I was also able to save about $500 off my tax bill.

I’d agree that was probably a smart move. It’s really hard to beat Vanguard’s fees.

My old work plan and my new 401k are both with Vanguard. The only reason I would not roll my 401k into an IRA with them would be if you make too much to contribute to a Roth in the traditional way. If you want to do a backdoor option, you’d have to pay pro rata funds on your IRA. Some brokerages will let you roll your IRA into a solo 401k so you can take advantage of backdoor Roths, but Vanguard does not allow that. This would only affect a small percentage of people, but if you are a high earner, its’ something to consider.

Since you and your husband plan to retire early, do you know if you’ll be able to access your 401k early (through a 72t/SEPP if needed)? Even if you don’t plan to use the money early, it would be nice to know that it will be an option without the interference of the employer.

In my eyes, a rollover makes sense most of the time. You have better access to your money, can invest for much lower costs, and add money to the account in the future. Plus, doing so lessens the chances that you forget about the account.

I couldn’t agree more. Unless there is a really compelling reason to stick to the 401k, the IRA rollover makes a lot more sense.

Thanks for all the great tips! I don’t think it’s a matter of if, but when! 🙂 But I like to see the “home” that everyone is choosing!

Vanguard is obviously my pick. Make your life simple and let them do all the hard work for you.

I rolled my 401K over into an IRA when I left my first job after college. The main reason I rolled it over was because I wanted to be able to access it if I needed to in an emergency. Like you mention though, the fees with my 401K were much higher than with the IRA I rolled it into.

Even for a first job after college, if its not that much money, I think it’s still a good idea and very responsible to roll it over. Putting your money all in one place where you can best management it – that’s just a smart idea.