If you’d like to use the 4 percent rule as your safe withdrawal rate but are terrified that it might leave you with nothing a few decades down the road, then I may have a great solution to offer you!

As I’ve been doing more and more research for my latest ebook (which will be all about optimizing “how much” you need to save for retirement), I’ve been getting really excited about some of the cool stuff I’m finding out.

For example, there was the post I did a little while back about how the updated Trinity Study showed that you could use a 7 percent safe withdrawal rate with a 91% chance of success if you don’t adjust your withdrawals for inflation.

The 1994 uber-classic 4 percent rule article from Bill Bengen also showed a 100% chance of success of your money lasting for 50 or more years if you used a safe withdrawal rate of 3.5% with inflation adjustment each year.

This got my creative juices flowing …

Why couldn’t we put the two concepts together and get the best of both worlds?

In this post, I’ve done just that. And I think you’ll be very surprised about how it appears to work out!

Doing More With Less

Before I get into the nitty-gritty details, I’d like to start off with the premise for this experiment.

Traditional retirement plans (such as the Bengen 4 percent rule) are usually designed to last for a minimum period of 30 years. If you’re like me and planning to reach financial freedom early on, this presents a problem. I need my money to last me 50 or 60 years; a lot longer than this.

An easy solution is to simply withdraw less money and lower your withdrawal rate. Like I mentioned above, Bengen’s article claimed that a rate of 3.5% worked every time for each 50 year rolling period. When I did my own study using FIRECalc, I found pretty much the same thing.

While that’s great to know, it does present you with a very significant problem: You need more money.

Half a Percent Makes a Big Difference

To illustrate this contrast, if I needed to create a passive income of $5,000 per month ($60,000 per year), then:

- Using a low safe withdrawal rate of 3.5%: $60,000 / 0.035 = $1,714,286

- Using the classic safe withdrawal rate of 4.0%: $60,000 / 0.04 = $1,500,000

That’s a difference of $214,286

That extra $214K is not so easy to come up with. Especially when your goal is to retire early, this means that you now have even less time to work with and leverage compounding returns to help you reach your goal.

Since we can’t very well find a magic investment that will yield a greater return than the S&P500, our only hope is to simply “save more money”.

Unfortunately, that’s easier said than done. I’m sure lots of people would like to experience financial freedom but forgot to start aggressively saving in their early 20’s.

As always, I ask the question: Can we do more with less?

A Possible Safe Withdrawal Rate Loophole?

Since we know that the Trinity Study supports a safe withdrawal rate as high as 7% without inflation adjustments and Bengen’s data supports a safe withdrawal rate of 3.5% with inflation adjustment, is there a way that we can compromise in the middle somewhere?

In other words, can I start my early retirement with a higher safe withdrawal rate if I’m willing to adjust less for inflation as time goes on?

If I’m able to do this, then I’d be able to start off with a higher withdrawal rate (which would require me to save less money in the beginning) and still have the safety and security of my money lasting beyond the standard 30 year threshold.

I had a few ideas about how I could test this theory.

Manipulating the 4 Percent Rule

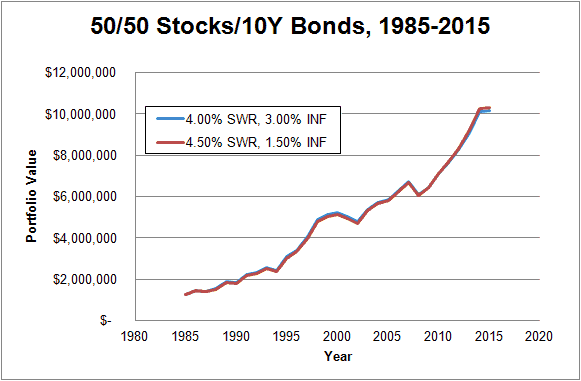

I started this experiment by downloading historical investment return data from NYU and setting up two main columns in Excel: One for a “standard” 4-percent, inflation-adjusted method and the other for what we’ll call a “hybrid” method.

Similar to Bengen’s classic approach, I looked back at 30 years of returns for a 50/50 split stocks and bonds portfolio with rebalancing each year.

Using the Standard method as a baseline, I started with a 4% withdrawal and then increased the withdrawals by 3% for inflation each year. Example: $40,000 the first year, $41,200 the second, $42,436 the next, and so on …

For the Hybrid method, I increased the withdrawal rate to 4.5% and decreased the inflation adjustment rate until the two graphs lined up.

At around a rate of 1.5% for inflation, the graphs were almost a perfect match with 2.2% or less variance!

My Finding: I was able to increase my withdrawal rate by 0.5% if I am willing to accept 1.5% less each year for inflation adjusted withdrawals.

Alright! We’re off to a good start.

Going for Safety!

So far so good for someone wishing to duplicate the standard 4-percent rule profile. But my heart was really set on duplicating the safer, longer lasting 3.5% safe withdrawal rate profile. Again, I know that if I can do this, then my money is virtually guaranteed to last for at least 50 years.

I then tried the same experiment again using a 3.5% safe withdrawal rate for the Standard and 4.0% for the Hybrid. Again, if I was able to reduce my inflation adjustment rate by 1.5%, then the two graphs line up almost perfectly with 2.3% or less variance.

My finding is the same as the last one!

Could I be on to something here?

The Problem With Lower Infaltion Adjustments … And a Solution

Before we go changing history with this new, revolutionary approach to the safe withdrawal rate, let me be the first to point out the obvious problem here:

Eventually you’ll reduce your purchasing power to an unacceptable level.

In my simulation, at first, the lower inflation adjustments are barely noticeable. But given the way that compounding returns work, that difference between the two rates gets wider and wider with time. By the end of 30 years (in the second experiment), the amount that the retiree gets to enjoy using the Hybrid method is 26% less than what a retiree using the Standard method receives: $62,523 vs $84,954.

If only there was some way to start getting additional money as we get older …

… Oh, wait. There is. It’s called Social Security.

Social Security’s Got Your Back

Despite what you may think, Social Security is not going away (completely) any time soon. Though they do report that after 2034 you will only receive 79 cents per every dollar of entitlement, that’s still several thousand dollars per year that you’re entitled to.

(Social Security can’t go away because if it did, there would be total social uproar. You and everyone else has been paying into it your entire working career. Of course, that’s to fund current retirees. Your Social Security will be paid by younger people who are working and paying in just as you are now. This is why Social Security is often regarded as one of the greatest legal Ponzi Scheme’s ever created.)

So then, let’s pay out the timeline. If you retire early at age 45 and start withdrawing Social Security by age 62, then you only had to live with the lower inflation adjustments for 17 years total. That’s really not that bad, especially when you consider the difference between Standard and Hybrid retirement income at that point is only 10%: $50,759 vs $56,165.

That’s really not that bad considering how much less you had to save to get there!

Conclusions

If you’re willing to compromise how much you’d like to adjust your retirement income for inflation, then mathematically it is possible for you to manipulate the 4 percent rule and enjoy a higher withdrawal rate while simulating the safety and security of a lower safe withdrawal rate profile.

For the two experiments I conducted, we found that you could increase your safe withdrawal by +0.5% if you’re willing to decrease your inflation adjustment by -1.5%.

I suppose you can have the best of both worlds!

This is yet again another tool that I will be considering as I update my financial freedom plan each year!

On a technical note: In the future, I would like to continue to develop this study by testing this theory against other rolling periods (for example: 1984-2014, 1983-2013, and so on). I’d also like to see the influence of other stocks / bonds ratios and how it holds up for periods longer than 30 years.

Readers – What do you think? Do you believe this could be the compromise between taking a higher safe withdrawal rate but maintaining a higher degree of safety? What are some other ways we could creatively compromise the 4 percent rule to do more with less?

Featured image courtesy of Flickr | Frankeleon

MMD, very interesting thoughts. Making your money stretch a little further will definitely help. It’s always impossible to say what the future returns of our investments will be, the one thing we can control are the expenses.

For us, we’ll try to get to a point where our retired-expenses are less than our investment income, that way we will never run out. There’s a whole investing community out there investing in Dividend Growth stocks where hopefully your income will keep increasing so there’s even less danger of running out.

Tristan

You’re definitely right that controlling your expenses is the main key; no matter what your strategy is. If you can make your expenses less than what your investments are producing, whether by dividends or also capital gains and interest, then I’m sure you’re going to enjoy a very long retirement … and have plenty to leave behind!

I just love how the PF & Investment communities try to think of ways to help each other. Definitely gave me some food for thought.

I’m not relying social security on my retirement calculations though. The whole thing is unstable. What if we go into another depression similar to the 1930’s one? What if we got into WWW III? I really don’t think the government will let go of social security as too many seniors depend on them but you just never know.

Life is so uncertain. I think social security will be a nice bonus, but it’s not going into my calcs at all.

Hi Lila! Welcome to the site.

I think a lot of people share your concern about the stability of Social Security. However, the chances of it ever going away completely are just too extreme. Literally millions of people who have paid into it since their first job at age 16 would take to the streets and skin the politicians alive. The more likely scenarios is that it will transform into something else; still to be determined what that is. But even that would still require a pretty radical transformation. Think of how many times they debated and shot down raising the eligibility age by a few years! For a total overhaul, there would have to be some pretty nasty circumstances.

MMD, a sound concept, as long as the reader realizes the importance of your point about a potentially lower standard of living in the future. The compounding effect of inflation is staggering, and must not be overlooked. I’m retiring at Age 55 (in 21 months), and just paid off the house. Therefore, I know my major living expense will be exempt from inflation (excluding property tax inflation). Health care inflation is the single biggest threat facing early retirees. I like your approach, but worry some will see it as an “easy out” without realizing the real cost of compound inflation until years later. Social security will help, but go in with your eyes open and continue doing annual checkups. Great article!

Thanks TRM! You are certainly right – there is a certain element of this approach as being like a crutch. If you can swing it, do it the real way and retire with 4% plus full inflation adjustment. Heck, use 3% and make it ultra-safe.

I like to explore / talk about these types of solutions because there are going to be a lot of people who will need the easy out. Sometimes when you read articles that perpetuate the 4% rule, the whole concept of retirement seems so far out reach. This is going to be problem because, like it or not, the vast majority of people are simply not prepared. I want them to know that there are other alternatives, but as we pointed out: There will be a significant trade-off.

Congrats on being on schedule to retire by 55! That’s got to be exciting!

After reading this post I realized how little time I’ve spent getting into the nitty-gritty of retirement planning. I hadn’t even heard of the 4 percent rule. I would like to focus a bit more on early retirement and lifestyle design, but it just hasn’t been a priority. Appreciated learning something new!

DC, I think you just gave me an idea for my next post: An introduction to the 4 Percent Rule!

I always cringe to use the phrase “retirement planning” when I write posts like this because I don’t want people to conjure up images of being old and in their 60’s. My intention is always to apply this knowledge somehow / someway towards early retirement and lifestyle design. My whole motivation for researching tips like this is to find ways to retire a few years earlier or pad our lifestyle with a few more thousand!

Good article. I see it simply as 3 windows that I tell my friends who check with me for their retirement advice. That is,

1. 3.5% initial WR or less means you can adjust by inflation every year.

2. 4-4.5% initial WR means you should skip inflation raises to alternate years.

3. 5% initial WR means you better be prepared to supplement your income by 50% in (bad) years where the withdrawal amount works to 6% or more of portfolio value.

First off, welcome to the site! I’m glad to hear you’re giving your friends financial advice. That’s what this whole thing is about; helping others.

I agree with #1. For #2, I think skipping / alternating inflation adjustments is simply a smart way to ensure the longevity of your nest egg. I see your point on #3, but do you have any data or numbers you’ve crunched to show this is true? I’d be interested to know.

I think if you are willing to save so much in your working years, all the while cutting back. That in retirement we all can find ways to cut back or find a enjoyable way to earn money. Playing with numbers is fun way to get you’re monte carlo on, but in reality doing with less and living simply is the real trick.

Well said! No matter what your plan is, if you’re willing to keep it simple, you’re setting yourself up for success.

Very interesting thought process on using the 4% Rule! Personally, I consider the standard 4% Rule 100% Safe… And for some of the reasons you explained above:

According to Bengen, it was 100% safe for up to 33 years. People often mix up Bengen and The Trinity Study. The Trinity Study was the one that gave the 95% figure.

I like your thinking. Another approach would be to simply step down your spending at a certain age. Say, 10% at age 75 and another 10% at age 85. Just watching my own parents (my Dad is 83), I can tell you they buy a lot less now than they did 10 or 20 years ago. They have everything they need and have traveled the world all they desire to. I’ve run the calc on our numbers and it makes a big impact.

Totally! Your observation about spending less later in life is one that’s been echoed by other financial researchers.

I think it could work in some specific situations. But decreasing inflation won’t work for a lot of people. I kept track of our expenses over the last 5 years and it fluctuated all over the place. We have a young child and that’s a big factor. Also, health is another huge factor as someone else pointed out above.

The stock market is also highly valued at this time. If you start out at 25x, you might be down to 20x in a year. There are too many unknowns.

I think everyone should use 25x as a baseline. Withdrawing more than 4% is too risky for me. I’d rather work part time and keep the withdrawal rate lower.

I can see your point, and I fully get that there is some uncertainty about how your spending your changes once you really are FIRE. I guess its safe to say though that your plan is only as good as how well you stick to it. Despite anything qualitative, the numbers still clearly show that even cutting back 1% on inflation could have its benefits. Lots of people go years without getting raises at their jobs and are already experiencing some form of inflation erosion without even realizing it. If you needed an extra edge, I think it could be a useful strategy to get you to where you need to be.

Honestly, I regret the fact that I didn’t start saving and investing in my twenties.. But I’m starting right now and that’s what’s important, right?

Big time! As it’s been said: The best time to plant a tree was 20 years ago. The second best time is now.

Another thing is to be flexible in your withdrawals. Most failures in the 4% rule are seen if one starts withdrawing in a crash. Taking out less when the market takes a plunge can greatly increase your survival. This might mean; no vacation, no new car, or house renovations for a few years but it might save you!

Absoultely! Both Bengen and The Trinity Study said the same thing; though no one ever mentions it. Being flexible with your withdrawals is critical to the success of your plan.

This was an intriguing article. I’ll admit I had an instinctive reaction to deny it could work, but your point about social security being your safety net is a good one. Still I have some reservations about falling behind inflation by about 1.5% every year. In 30 years, I would basically be living on 2/3 of equivalent real dollars due to the inflation outstripping me. I’m not sure my budget has that much fat to cut.

Given that the first ten years of a retirement can predict with 80%+ accuracy the success of retirement (sequence of returns), what do you think of controlling the spending in the earlier years instead when you are healthier and have more visibility? I wouldn’t propose a 30% cut in budget for ten year of your prime living years, but Bengen has also talked about a variable spending strategy with a floor of 15% where you cut your spending by 15% in bad years and raise it in good years to a ceiling of almost 20%. It allows you to increase your SWR by about half a percentage point as well but may be more palatable. Curious to get your thoughts.

Pretty much all the data out there from Kitces, Pfau, and others suggests the first 10 years are critical! I’ve also heard of the latter Bengen strategy you mentioned. Though it would be smart to start off your FIRE by withdrawing as little as possible to ensure those first 10 years are a success, I find two challenges to this:

1. I think the first time people finally become FIRE, what becomes of their lifestyle is a wildcard. Some people will show restraint and stick to the plan. Others won’t. If you really wanted to build yourself a safety margin, I’d actually plan to spend more in the first 5-10 years. But, of course, not more than the upper limit that this research suggests.

2. We don’t know how Mr Market is going to behave. If we have a series of down years, then the ride could be rough – even if we do show restraint in our spending. About the only tool we have to get some indication is to look at the Shiller CAPE to see (in general) if the market is currently over or under valued.