As parents, we want our kids to have the best. We want them to be happy, healthy, and successful in life.

And one of the best ways I can think to help aide them in building security is to set them up on the path for financial excellence from an early age.

This of course does not mean winning the lottery or transferring over your wealth. I’m talking about passing on the knowledge and skills necessary to help build wealth from scratch over the long haul.

With both of my children becoming teenagers and (within the blink of an eye) young adults, I’m thinking about this topic more and more.

In particular, I’m trying to decide how best to present this information to them in a way that sticks forever.

After some careful thought (and what I would consider a lot of generosity), I have an incredibly simple strategy that I think will work really well at setting both of my children up to potentially become millionaires! Not only will it help educate them first-hand as to how money actually works, but it could also help give them a BIG head start on their own paths to financial freedom.

In this post, I’d like to share my plan with you. Perhaps if you’ve got children (of any age) too, then this strategy might be of some value to you and your efforts to help them out with money.

Starting a Roth IRA at Age 16

Anyone who has ever played around with a financial calculator or anything that computes compounding returns knows that the earlier you start investing, the better off your chances for success are.

Of course, investing is tough when you’re a kid. The only money you usually earn is what your parents pay you. And even then, you usually want to use it for fun stuff anyways.

When I think back to my early financial situation, one of the biggest changes for me happened when I got my first job at age 16. I went from making a $5 allowance from my Dad to suddenly receiving hundreds of dollars from the restaurant I was working at every month.

As a natural saver, I was good about putting a big majority of that money in the bank. But if I could go back in time, I would tell myself to take it one step further. And so this is the advice I plan to pass on to my kids: Start a Roth IRA!

Let’s look at the simple facts that come with Roth IRA’s:

- First off, to even contribute to a Roth IRA, you need to have earned income. Therefore, their first part-time job will qualify them.

- Since this is a Roth-style account, they will pay their taxes now rather than later on in life. That’s great because when you’re 16 earning a part-time wage, you’re probably going to be in the lowest tax bracket of your whole life.

- Any money that grows on top of this money will be tax-free from now until forever.

- Starting a Roth at age 16 will also help them to get an early jump on the five-year rule for taking Roth IRA contribution withdrawals; just in case they ever need them later on in life.

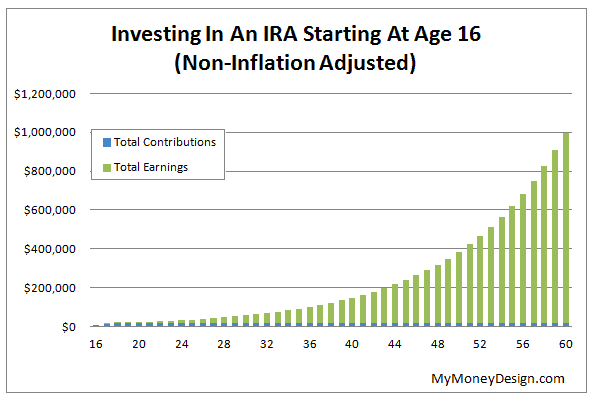

To get started, let’s assume for one second that they invest the maximum amount of $5,500 per year into their IRA at age 16, 17, and 18. The money is invested in a stock market index fund earning an average annualized rate of roughly 10% (according to data from NYU).

At first, these 3 years won’t seem like much of anything has been accomplished.

But then, the longer we wait, the biggest benefit of starting early begins to kick-in: Compounding returns!

Compounding returns cause your earnings to grow exponential. Look at any graph involving compounding returns, and one thing will be clear: If you would have started earlier, there’s a great chance you’d be FAR MORE richer!

… this is where the beauty of this strategy lies! By starting at age 16, that’s almost 9 years before when most young professionals even start to think about saving and investing.

So – how much would those simple 3 contributions of $5,500 add up to by age 60 (44 years later)?

$996,973 – almost one million dollars!

(Of course, that’s without inflation. With inflation, this money would actually only be worth about $303,144 by that time. Not bad … but we’ll fix this problem in the upcoming sections.)

My Offer to Turn My Kids Into Millionaires

This all sounds good in theory, but how do you get a teenager to contribute $5,500 to a Roth IRA – especially when (to them) it feels like retirement is a billion years away?

My plan is simple: Make them an offer they simply cannot refuse. I will offer to match them dollar for dollar what they contribute to their IRA (combined up to the IRS max). In other words, if they contribute $2,750, I’ll kick in the other $2,750.

By IRS rules, this is perfectly legal so long as they actually earn $5,500 or more. If they earn less than this level, then that number becomes the new maximum level.

This will be sort of like when employers match your 401(k) contributions. I will use it as a way to heavily motivate them to save more and more – in addition to the prospect of one day having a physical balance of almost one million dollars.

But beyond that, this will also help them get the right footing for investing at a very early age. They can learn about mutual funds, index investing, and capital gains. Not to mention they will also see first-hand how investments can rise and fall with time.

Continuing to Encourage Financial Habits

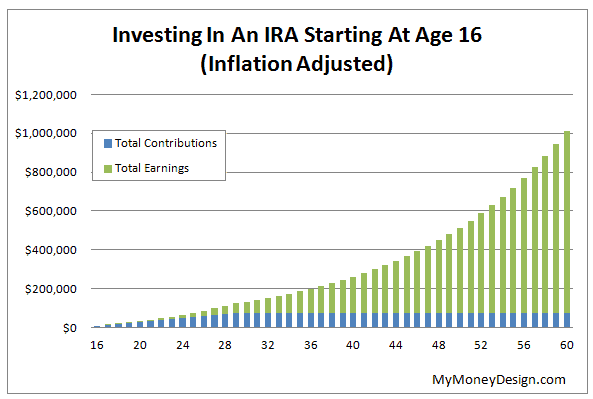

So how can we develop this further into one million dollars of real, inflation-adjusted money in the future?

In order to do this, we will need to continue the process of investing $5,500 into their IRA for a total of 14 years (until they are age 29). By this point, their growth potential will be $1,010,219 with inflation adjustment (or $2,953,288 in nominal dollars).

How can I help ensure they invest?

During the college years, I could continue to make them the same dollar for dollar match into their IRA’s.

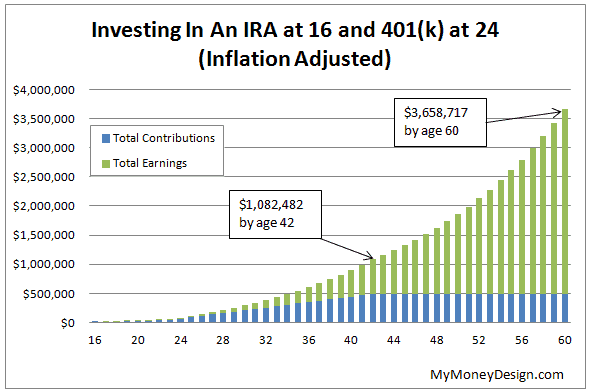

Hopefully by the time they graduate and get their first real job, they can then start making their own full contribution to the IRA. My bigger hope of course, is that by this point they realize what a golden financial opportunity this is and take even more advantage of it with their 401(k) plans as well.

In fact, if they did, becoming a millionaire would happen quite a few years sooner! Here’s what that same graph would look like if at age 24 they started contributing the max to both their 401(k) and IRA (up until they reach $1 million at age 42). (… yes, I know a young person investing that much that early is a stretch, but let’s just run the numbers and have some fun imagining the possibilities! …)

Conclusion

What’s not important here is whether or not they actually make it to one million dollars. As you probably know – what each person needs to be financially independent is as unique as the individual.

What is important is that I draw them into a world where they see opportunity. Putting compounding returns to work for yourself at such an early age is a ticket to wealth that not many people are given. It’s truly one of the most intriguing and passive ways to build your wealth. Hopefully my offer entices them to make the correct decision!

Readers – Do you have any plans for turning your kids into potential millionaires someday? If so, how do you plan to do this? What sort of lessons or strategies will you be using?

Featured image courtesy of Pexels

My children are younger than yours, so we have some time to develop a plan, but I really like this idea. Thanks for sharing it!

Thanks! Hopefully you can borrow this strategy to use for your own someday.

My plan to help my kids achieve financial security is the same one my parents used. My kids will, if capable, graduate from a state university with no debt and with a used car. Hopefully they get a nice inheritance 10 years or so before they retire.

These days, that’s putting them in a better financial position than about 99% of their peers. There isn’t a 20-something I know that doesn’t have or had student loan debt.

This is awesome, I love the match proposal you will offer your kids! We have a 2 year old, but I think we may need to consider this strategy in 14 years!!!

Can you imagine how cool it would be if you started this trick at age 2? 14 extra years of compounding returns! Though totally impractical, its fun to run the numbers and see how crazy they would get.

This is a fantastic idea, and it adds on to what I’ve just done recently with my 12 and 13 year old. They’ve begun “working” now, as soccer referee’s for our rec program in town (they make ~$20 on a saturday). My bargain with them is if they save at least 50% of it, they can put it in the Daddy 401K and I will match it dollar for dollar. It’s expanded into birthday money, allowances etc. My daughter just surpassed $500 and she asked if she can buy stock with it. I might have to create a separate account in my sharebuilder account for her. Once they have a “real” job, I am going to offer this to them as well.

I LOVE it! The Daddy 401K. That’s brilliant. That’s really incredible that your daughter has already saved up so much and is asking about stock. You’ve definitely got them off to a great start.

Very interesting post DJ. Interesting to me BECAUSE, I very recently started to explore this topic with my oldest son (10) and sort of with my next son (7). I want to teach them how to handle money and be ‘rich’ – except my mindset is totally different thanks to some books I’ve read recently by Robert Kiyosaki.

I’m sure you’re read, ‘Rich Dad, Poor Dad’ – I read that book about 8 or 9 years ago. Right before I started internet marketing. And I just re-read it last month! Great book and that is what motivated me to start teaching my kids at a young age, I even bought one of the kid versions of that book for them to get started with!

But… even more recently I read another one of Robert Kiyosaki’s books. It’s called, ‘Rich Dad’s Who Took My Money?: Why Slow Investors Lose and Fast Money Wins!’

What an eye opener this philosophy is! Bottom line… other than just ‘investing for the long term’ (which is what that book states is terrible advice) – I’m going to be teaching my kids all about money and how it works. Owning an entrepreneurial business will (by far) be their best shot at ‘getting rich’ – I want my kids to be rich and financially free when they are young. Not just old rich millionaires ‘someday’…

But at the same time – I DO want them to understand the power of compound interest and have them set away some savings as a safety net (like your post suggests). The point is – becoming a millionaire someday is nice – but learning how money works and how to handle money and how to get rich is more exciting and probably more important in today’s world. I highly suggest you read that book to get another perspective…

I’ve read a couple of Kiyosaki’s books now, including Rich Dad Poor Dad ( … I think it may even be a prerequisite to starting a personal finance blog … LOL). I can definitively appreciate Kiyosaki’s philosophy for entrepreneurism and there is a lot of great advice in that area. However, he’s got it all wrong when it comes to investing for the long term. Not taking advantage of market appreciation and the power of compounding returns is simply passing up a good thing. The average annualized growth rate is right around 10%. Plus when you factor in the ability to defer taxes with your retirement accounts and get employer matching, that’s just even more money that’s left on the table for anyone that follows him on this point.

I like that strategy, offering to match dollar for dollar what they contribute to their account as a teenager, I will definitely borrow that strategy, though I have a bit of time before my little one reaches adolescence.

Great post!

It’s there for the taking anytime! I’m glad you liked it.

That dollar for dollar match is a hard offer to pass up!

I have two kids, my daughter is pretty ambitious and has told us many times that she would like to own a big house one day. My son is the total opposite and although he cares about money, he’s also said a few times that there is really nothing wrong about being poor. We’re working with his mindset consistently. Great post by the way.

Thanks Bernz JP! Our family lives in what I would describe as a pretty big house and we always joke with our two kids: Don’t buy a big house! A big house just means more cleaning, more lawn work, and more things that break / need repaired!

Found this post via link from one of your more recent posts. Great idea!

I had paper routes and babysitting as a 12-15 year old and had amassed around $3,500 in my savings account. It was my dad who suggested starting a Roth IRA. I put away what I could in college, but didn’t quite get this consistent early bump (it surely wasn’t $16,500 by the time I started my first job). Even so, that early bump did help. And, it taught me the advantage of having a non-taxable account, compound interest, and peaked my interest in the idea of retirement savings at a young age. Also, anyone reading this blog probably at least talks about money at home, so that’s a huge start over many families. Even though my parents weren’t able to do a match (or maybe didn’t have the idea), it still is a great idea to introduce at a young age.

I’m forgetting, but I’m guessing the Roth wouldn’t alter a FAFSA for student aid? Seeing as they haven’t gotten to post-secondary yet.

Have you ever considered “angel investing” in any kind of entrepreneurial projects they have? I’ve always thought that was an interesting concept to try to spark that entrepreneurial spirit.

My kids are young, but I’m starting a “savings” fund for these types of things. Obviously, doing some short-term investing to grow that until they are ready for things. But, basically we move the money we use(d) for daycare (a lot) to a new account for additional college savings, activity fees (music, camps, athletics), and maybe these kinds of matches in the future. In other words, “kids” in the budget is always the same (and probably increases). Ha.

My grandfather was a big proponent of this! He didn’t require a match, but rather our time to be trained.. Back when I was a teenager he would invest up to $2000 (the max at the time) in an IRA for any teenage grandkid with W2. That gift came with lots of discussion and education. That $6000 he contributed to my own IRA is now worth $160,000 and growing strong!