That was the question I received when I was trying to help someone pick some mutual funds for their 401(k) plan. It’s definitely a good one to ask!

Over the years, a seemingly growing number of academics and financial bloggers have really been showing their love for investing with passively managed index funds (myself included). With all the major advantages and benefits they point out, it sure seems like a no-brainer that this is the way to go.

Yet, when you take a closer look at where the money is actually going, it may surprise you to learn that the numbers paint quite a different story.

In the US, some $9.8 trillion in assets sit with actively managed funds. How much are with passively managed funds? Only $4.2 trillion. This means that as a whole, 70% of all US investments are held in active funds.

As someone who personally believes in index fund investing and holds most of his retirement portfolio in passive funds, I have to ask the question: What’s going on here? Do active fund investors know something that the rest of us don’t? Is there something that passive fund enthusiasts are missing?

Or is there more to it than we know? Could people be pouring their money into active funds and not even know it?

Let’s explore the facts from both sides of the passive vs active fund debate and see what we can learn from all of this.

First – Why Has Investing In Passive Index Funds Become So Popular?

I think it’s appropriate to begin any conversation about index fund investing with the man who popularized the idea: John (Jack) Bogle.

In 1974, Bogle started the company The Vanguard Group and offered the first index fund publicly available. At the time, it was called “Un-American” and nick-named “Bogle’s folly”. But eventually, things caught on. Vanguard is now the world’s largest provider of mutual funds. There is even a cult-following of financial enthusiasts who call themselves the BogleHeads.

Bogle’s Philosophy

The rationale behind investing in index funds can best be summed up from something said by Jack Bogle during his speech at “The World Money Show” back in 2005:

“Most people think they can find managers who can outperform, but most people are wrong. I will say that 85 percent to 90 percent of managers fail to match their benchmarks. Because managers have fees and incur transaction costs, you know that in the aggregate they are deleting value. The investment business is a giant scam.”

Wow, those are some pretty strong claims! Let’s break this down into a few key take-aways:

“85 percent to 90 percent of managers fail to match their benchmarks.”

In other words, professional money managers whose sole job it is every day to understand the finances of the companies they pick and invest our money in can’t out-smart the market.

Furthermore, if you read between the lines of this statement, what Bogle is basically saying is that if the pros can’t even pick the right investments, then how can we ever expect to do so?

We can’t. And neither can most pros.

Therefore, we could all expect to save ourselves a lot of time, trouble, and effort if we just invested in an index fund instead.

“Because managers have fees and incur transaction costs, you know that in the aggregate they are deleting value.”

It is certainly true that active funds cost more than passive ones. According to an article from The Balance:

- The average Large-Cap Stock Fund costs 1.25%

- The average S&P 500 Index Funds is priced at just 0.15%.

(… Actually, the Vanguard 500 Index Fund Admiral Shares offers the lowest known expense ratio of just 0.04% (if you invest $10,000 or more). That’s literally only $4 in cost for every $10,000 you have invested!)

So what’s the big deal with fees?

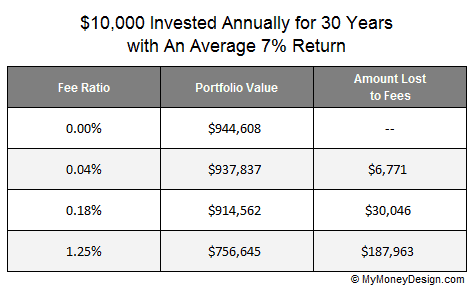

0.04 and 1.25% may not sound like two numbers with a big difference. But when you look at how they can compound and impact your earnings over time, the results are HUGE – as in six-figures HUGE!

Just doing a simple projection of $10,000 per year invested for 30 years with 7% average returns, you can easily determine how much you’d lose to fees: A difference of $181,963 to be exact … Yikes!

Why are active fund fees so much higher?

Because paying someone (or group) to “actively” manage a fund costs more. You’ve got salaries on top of more overhead with trading costs, research, analysts, and so on.

Right or wrong, at the end of the day, this just means more money coming out of your pocket!

So in summary, Bogle feels you’re getting hit from both ends. Not only are you not making as much at the top with the kind of returns that passive funds produce over the long term, you’re also getting chopped down from the bottom with higher fees. He paints the picture as pretty much a lose-lose situation.

So if Bogle’s statement is true, then why do SO MANY people still invest with actively managed funds?

401(k)’s Are Littered with Actively Managed Funds

Do you have a 401(k)?

If you do, go to the section where you pick your investments and tell me what you see?

If you said “a whole bunch of actively managed funds”, then I’m afraid you’re not alone.

In my own employer’s 401(k) through Fidelity, we have 57 funds we can choose from. Only 4 of them are passive.

I’ve heard this same complaint from many different people across the Internet. In some cases, their plans offer NO passive funds at all.

Is This a Coincidence?

The total size of retirement assets in the US was $25.3 trillion at the end of 2016. This works out to 34 percent of all household financial assets in the United States.

Defined benefit plans such as 401(k)’s work out to $7.0 trillion of this pie. If the average actively managed fund charges just a 1% fee per year, this works out to $70 billion in revenue annually.

1% might even be putting it lightly! At my previous job, one of the funds in our 401(k) plan charged over 2.0%! That’s complete B.S.!

To put it simply: 401(k) plans are a big business! This is why most of them are made up of actively managed mutual funds – because they can charge more for them then passive funds. And the more they charge in fees, the more money they make.

This is one of the major reasons why 401(k) plans are often vilified by the public. It’s questionable whether some of the funds they offer are really even any good or not. Are they simply there just to collect a cut of the high fees? Who’s best interest is really being served – the investor or the financial company?

This reminds me of a wonderful story that beautiful sums up the situation. It comes from a book called Where Are the Customers’ Yachts? by Fred Schwed, and was published over six decades ago. Here is the story as paraphrased by The Motley Fool:

“The title came from a story about a visitor in New York more than a century ago. After admiring yachts that Wall Street bankers and brokers bought with the money they earned from giving financial advice to customers, he wondered where the customers’ yachts were. Of course, there were none.”

But if some 401(k) plans do contain passive funds, then why wouldn’t people choose them?

Again, let’s use my own 401(k) plan as an example. With all things being equal, when the average US retirement saver goes to pick his funds, there’s a 4 in 57 chance or 93% probability that he will choose an active fund.

According to a wealth adviser from this article with CNBC, this is unfortunately what A LOT of people do – randomly choose their investments. The sad position that we are in is that the average American saver is not necessarily educated enough about personal finance to really know what makes one fund choice better than the other.

Over the years, I can’t tell you how many people I’ve personally talked to who have picked the funds in their 401(k) plan without any discernible reasoning whatsoever. Maybe it was strong returns the year before, a high Morningstar ranking, a nice sounding name, … any number of variables. But few of them ever on the basis of whether the fund is actively or passively managed.

In other words, “the deck is stacked” in favor of active funds.

While this might be a major factor for the common investor, what about everyone else? What makes up the other trillions of dollars being poured into actively managed funds?

I believe the answer is quite simple.

People Want Actively Managed Funds

Believe it or not, there are a staggering number of people out there in the world who simply do not want to settle for “average returns”.

They want to do better! And if that means paying a little extra for an actively managed fund, then so be it!

Index Investing is a Relatively New Concept

When you put this in perspective with how Americans have been investing over the last few centuries, I think it makes a lot of sense.

- 1792 – In the United States, the first major stock exchange, New York Stock & Exchange Board, is created. Investors can now pick which companies they believe will succeed and become the most profitable.

- March 21, 1924 – The first modern-day mutual fund, Massachusetts Investors Trust, begins. Investors can now easily diversify and let a fund-manager do all the hard work of picking the best stocks to make them wealthy.

- December 31, 1975 – John Bogle creates the First Index Investment Trust (later renamed the Vanguard 500 Index Fund) one year after starting The Vanguard Group.

Relatively speaking, index investing is a “new” way of thinking. For literally hundreds of years, it’s been engrained in the minds of both professional and casual investors that getting rich means picking the right stocks. They have high-hopes and intentions of putting their money into something (or with someone) that will deliver above average returns.

(Coincidentally, this is also why more financially affluent investors choose to go with hedge funds. Again, they are doing so on the promise, or hype, that they will receive above average returns.)

So are those who invest with actively managed funds just being foolish?

A closer look at a few results may not seem to suggest so.

Active Funds Don’t Always Fall Behind Passive Ones

Bogle’s comment is that most actively managed funds fail to beat their benchmarks. Keyword being “most”.

To be fair to any of the “good” active managers out there, their priorities are not always the singular goal to simply “beat the market”. The most responsible ones will also find ways to minimize risks during periods of economic turbulence.

This two-prong approach is how some funds are able to beat their benchmarks for periods of 10 years or more.

Vanguard Example:

“Vanguard’s Windsor fund is an active fund that has beat a passive fund in a 39 year stretch. If $10,000 were invested in it from August 1976 until March 3, 2015, it would have grown to $967,947 versus $581,814 for Vanguard’s S&P 500 index.”

Hallam then goes on to list several other Vanguard active funds which have beaten their index over a ten year period from 2005-2015.

For US Large-Cap, active funds beat the index funds 7.74% vs 7.69% after tax.

This was also true for International stocks: 5.17% vs 4.35%.

(Of course, to be fair to the passive funds, Mid-Cap, Small-Cap, and Bond indexes beat their active fund counterparts. All-in-all, the numbers were relatively close.)

T-Rowe Price Example:

Of course, those are very specific time-periods. T. Rowe Price did a little more comprehensive approach of active versus passive funds in their post “Long-Term Benefits of the T. Rowe Price Approach to Active Management“.

Their study examined performance over rolling 1-, 3-, 5-, and 10-year periods (rolled monthly) from 12/31/1996 through 12/31/2016. Returns were net any fees and trading costs.

What did they find?

“Half of the funds (9 of 18) outperformed their benchmarks over every rolling 10-year period, while two other funds outperformed in at least 98% of their rolling 10-year periods.”

Berkshire Hathaway Example:

Okay … Okay … So Warren Buffett’s Berkshire Hathaway isn’t technically an “actively managed” fund the same way a mutual fund from Vanguard is. But here me out. In essence, buying this stock works out to be pretty much the same thing: You put up the money, Warren Buffett and Gang pick the companies for you to invest in, and you all get rich!

How rich?

In a 2016 article from Yahoo Finance:

“Since 1965 to December 2015, Berkshire’s shares have returned 20.8% per annum for a cumulative gain of 1,598,284%, compared to an overall gain for the S&P 500 with dividends included of 11,335%.”

When compared to the roughly 10% return of the S&P 500, 20.8% is not too bad at all!

Not All Active Funds Are Expensive

If high fees over 1% are one of the main criteria that makes actively managed funds “bad”, then would you still feel the same about them if you found some with really low fees?

Do those exist?

Of course they do. Part of Vanguard’s success was built on the reputation for having some of the lowest fees in all of investment service industry.

How low are we talking?

According to their own site, Vanguard’s average expense ratio is 0.18%. That’s quite a bit different from the average industry rate of 1.25%.

Furthermore, their active fund average price works out to just 0.14% higher than what they charge for the Vanguard 500 Index Fund (admiral shares). Using the same 30 year projection we did before, that only works out to a difference of $23,275; a lot less than the $181,192 we calculated with the industry average.

Bottom-line: With fees that low, it completely levels the playing field. Now you can make your decisions based on performance and asset allocation.

Asset Allocation Goals

One of the big criticisms of index fund investing is that it does not necessarily coincide with the specific asset allocation goals and risk profile that some investors hope to maintain.

For example: X amount in a certain group of stocks, Y amount in certain type of bonds, etc.

Sure … you could just buy other index funds in an attempt to create the type of profile you’re after. But now you’re doing all the juggling to make sure those funds are properly maintained and balanced every year.

This is yet another reason why some people choose to pick actively managed funds over passive ones. They WANT someone to manage this asset allocation balance and risk for them.

And as long as we can find a fund that A) the performs well over time and B) carries low expenses, is would this really be such a bad purchase?

Two examples I can give you are two of Vanguard’s old chestnuts: The Wellington and Wellesley funds. Both are well-known balanced funds offering specific types of asset allocation. The Wellington is about 2:1 stocks to bonds with diversification across a number of prevalent sectors. The Wellesley is 1:2 stocks to bonds with a focus on dividend paying stocks with a proven historical track record.

When you account for both stocks and bonds, each of these funds has beat its composite benchmark over the long haul. And with expense ratios of 0.25% and 0.22% respectively, this is still only a small price to pay above what investing in a simple index fund can do for you.

What Can We Learn From All of This?

In summary, I believe we can conclude the following.

Yes, there are a lot of clear benefits to choosing passively managed index funds over active ones. Their long-term performance and low costs combined with their simplicity make them a terrific staple for any level of investor.

If you want to keep things simple and invest without the fuss, then just go for all passively managed index funds.

But be careful not to paint all actively managed funds as “bad”. Not all of them are.

True: It sure seems like a common complaint of many funds being offered in 401(k) plans across America is that they do not perform well and charge outrageous fees for the brokers who offer them.

But that doesn’t mean that there aren’t any “good” opportunities to be found with actively managed funds. Like all investments (stocks, real estate, business, etc.), you have to put in some work and effort to find the right ones. This would mean doing some research, learning about what the fund consists of, how it has performed against its benchmark over long-term, what kind of fees it charges, and what kind of diversification it can offer you. In the end, it may just end up being a good fit for you and your money.

Readers – Why do you think people continue to invest in actively managed funds? Can you think of any other times when there can be an advantage to what they have to offer? How can aspects to both management strategies be used to create the best investment profile possible? Fair warning – please keep the discussion constructive. Any comments that attempt to bash one side or the other will not pass moderation.

Images courtesy of Flickr, Flickr, and FreeDigitalPhotos

I think most people choose active funds because they want to beat the market. People for whatever reason have competition instilled in them and these brokers (salesmen) convince them that they can beat the market. I have to admit I use to try to beat the market year in and year out. I was delusional and have moved over to passive index funds at this point. I’m doing really well now 🙂

I totally hear you! After years and years of thinking I could out-pick and out-calculate the market, the market wins. Putting the majority of my savings into passive funds is just easier.

Passive investing is the way to go. I even consider dividend growth investing to be passive because you ideally aren’t constantly trading in and out of positions. Just buy at a good price and collect/reinvest those dividends.

When it comes to the retail investor, I think most people don’t even know that there is an active/passive divide. We finance bloggers know about this, but it’s all Chinese to most people. Combine not knowing the difference between a mutual fund and an index fund with people not knowing how the stock market always grows over time (“The stock market is random and gambling! You’ll likely lose all your money! Who knows what can happen!?”), and people would rather let “experienced professionals” make the decisions for the rather than let the market itself decide. Because in their minds, the market is a black hole that will just suck up their money, never to be seen again.

Sincerely,

ARB–Angry Retail Banker

This is precisely the type of thing Jack Bogle is speaking to: The people who prey and lurch onto those who are not as financially savvy as the rest. Unfortunately where there is fear and/or ignorance, there will be always be those who will take advantage of these vulnerabilities. The common adviser would do well to (at a minimum) become educated on the benefits of index funds and then just stick to them. At least in this way they could smell a rat whenever someone tries to tell them differently.

Interest read. Thanks for sharing! Passive funds may sound great because it implies you don’t have to do much but can still reap the benefits. But the management fees can be ridiculously high sometimes.

That’s why I like to stick with someone like Vanguard. 0.04% is about as low as they come!

Hi MMD, first time commenting on your blog and just wanted to say thanks for all the work you’ve put into it! Yours was the first FI blog I started reading (even before MMM and the Mad Fientist), and it’s what started me on the path to FI!

Anyways, well researched article – I never thought about a 401k as being a business. I definitely think that people choose actively managed funds in order to beat the market. It’s tempting to try and “get rich quick.” A lot of what people do seems to be because it’s what they’re “supposed” to be doing, but they don’t really understand it. I think that’s another reason people choose actively managed funds – not enough understanding or desire to gain that understanding.

Personally, I’m ok with getting average returns and I’ll be sticking with passive index funds.

Hi Matt!

Thanks for the compliments and welcome to the site! I’m honored to mentioned among such other great blogs.

You’re totally right. I think there’s a definite mentality that picking stocks is the “right way to go”. People think they can beat the system, and some of them certainly do. But unfortunately the majority of us never will; at least not for any sustainable amount of time. Personally, I’m with you and would rather just opt for the average returns. At least then my time spent on picking investments is minimal, and I can put my efforts into figuring out other strategies like tax savings and frugality hacks. Plus, average returns aren’t really so bad – not when they’ve been averaging 10 percent-ish for the past 50 years or so.