After reading enough personal finance blogs, this whole financial independence thing starts to sound pretty good! But what exactly are the steps to retire early?

How does someone acquire enough money to never have to work again (if they choose)?

What was the path that got them there?

And more importantly, what are the habits and routines in our daily lives that we can adopt that will help make early retirement an option?

You might be surprised to learn that much of achieving financial independence has less to do with earning a lot of money and more to do with how you go about getting it.

Your ticket to freedom doesn’t necessarily have to include some fancy high-paid position. Although it might help accelerate things a bit, the steps to retire early are fundamentally the same whether you earn $50,000 or $500,000.

What it should include is discipline and the ambition to squirrel your money away in all the right places.

In this post, we’ll organize each of these tips into 10 steps that will give you the most bang for your buck.

1- Make Your Financial Education a Priority

I’m always amazed at how much the average person can tell you about their favorite sports team or beer. But then it comes to knowing the difference between a 401(k) or IRA, they have no clue.

The path to early retirement isn’t something that happens causally. In order to properly plan the right strategies and then know how to execute them, you need to become a bit of a black-belt in personal finance. And that means putting forth some effort in your own financial education.

The best place to start is to read at least one good book about how to manage money. In particular when it comes to the topic of early retirement, one that I really enjoyed was “How to Retire Early” by Robert and Robin Charlton. It’s the story of how a couple was able to retire in their early 40’s after going from basically nothing to one million dollars of savings in just 15 years!

Of course, if you’re just getting started, our “Start Here” page on this blog can also be great place to find a ton of organized information.

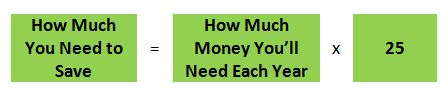

2- Know Your Savings Target

No one ever just gets on a plane and flies somewhere random. They have a destination; a place they intend to go to.

The same is true of retirement. And when going after early retirement, it’s extremely important.

The easiest way to figure out your retirement savings goal is to start with the 4 Percent Rule. This would be the amount of money that you pull out of your savings every year to live off of passively. To figure out your savings goal, simply divide your desired income by 0.04 or multiply it by 25 (mathematically its the same thing).

Example: I want to retire on $5,000 per month. That’s $60,000 per year. Therefore, to find my nest egg savings target, I multiply $60,000 x 25 = $1,500,000.

If you want to retire younger than 50, then I’d suggest you replace 4.0% with 3.5%. (Or you can multiply your target income by 29 instead of 25.) The reason is because the younger you retire, the longer you will need your money to last. So by starting with a lower withdrawal rate, you’ll increase your chances for success.

3- Start Saving Yesterday

Okay … obviously you can’t do that. But hear this …

There’s an old saying that goes: The best time to plant a tree was 20 years ago. The second best time is right now.

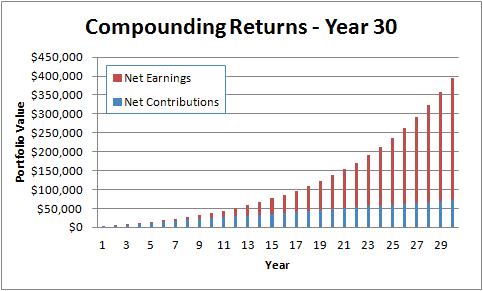

In terms of personal finance, this is talking about the power of compounding returns. Leveraging “time” to let your investments grow is one of the most effective tools that any saver has.

It can lead to returns that FAR surpass anything they could have saved on their own. If you don’t think so, just look at this graph here.

So even though you can’t go back in time and start saving, make no excuses for today. Start putting away as much as you can, and keep doing it regularly. As your returns start to stack up and grow, you’ll be glad you did.

4- Simplify Your Investing With Funds

Forget trying to chase after high yields. Forget complex asset allocations. This is a fools’ game.

When it comes to knowing the best funds to pick, stick to the index funds.

In case you don’t know what those are, an index fund is an investment that simply tracks the market. Basically, you always earn whatever the average market has earned; no more and no less. While that might not sound very sexy, over time this strategy has proven to be incredibly effective – especially for newbie investors!

In terms of diversification, some financial experts recommend as few as two types of index funds: One for large-cap stocks and one for bonds. While you’re in the saving phase of your progress, invest heavily into the stock index fund. Even though it will be more violate than the bond fund, it will provide you with the greatest chance of success over the long run. If you’d like to see for yourself, just check out the S&P 500 returns over the past few decades.

5- Save As Much As Possible Every Year

Again: Scrap the idea of trying to chase after some stock or fund that’s promising higher returns.

Believe it or not, the biggest part of your retirement plan that you have complete control over is how much you choose to save. And therefore, you should do everything in your power to put away as much as you can afford.

Think about it this way: Instead of taking an unnecessary risk to try to get an extra 1-2% return, why not just find a way to simply save another $1,000 or $2,000 this year? That way, you’re guaranteed to increase your savings by that much.

And the more money you save, the more volume those compounding returns have to work with towards producing bigger returns.

6- Take Full Advantage of Tax-Advantaged Savings Plans

If you’re putting your savings into the bank or a regular brokerage account, you’re doing yourself a great disservice.

A 401(k) or IRA is far superior to regular taxable accounts for one big reason: tax-deferment. Your ability to save your money before taxes are taken out gives you a 33% edge over regular systems of saving.

Consider the math: Normally $1 earned is really about $0.75 net to you after 25% taxes. But when you use a tax-deferred savings plan, the whole $1 is saved. That’s $1 / $0.75 = 1.33 = 33% more!

On top of this, tax-advantaged savings plans also shield you from having to pay taxes on your earnings every year when you move funds around or receive dividends. That’s just more savings for you!

7- Get All the Free Money You Can

Tax-advantaged savings plans aren’t the only break the IRS gives you. Make sure you also take advantage of these awesome perks too:

- Most employers will make matching contributions to your 401(k) plan; sometimes dollar for dollar. That would be the easiest way ever to get a 100% return on your money – tax deferred too! Find out what your employer offers and then do everything you can in your power to take advantage of the full match.

- Flexible savings plans are a way for the employees to get a similar tax break on medical expenses and dependent care expenses. If your employer doesn’t offer them and you have high medical deductibles, you might be able to qualify for an HSA

- 529 plans are very similar to IRA plans but with the purpose of saving for your child’s college expenses instead of your retirement. Tax breaks while saving for your children’s future means more savings available to you to put towards your own retirement.

8- Learn to Live on Less

If you’ve ever calculated how much money you thought you needed in your nest egg to retire early and said to yourself: How will I ever save up that much?

The answer is that you might not need to.

Retirement planning is a double-ended approach. On the back side, you save up a bunch of money towards a nest egg goal that you hope to have in the future.

But on the front side, you can learn to discipline your lifestyle and not need as much as you might think. This will in turn lower how much money you’ll need in retirement, and thus lower your nest egg target goal overall!

This is actually how many early retirement bloggers have accomplished their goals at such a young age. The classic example is of Mr. Money Mustache who got his annual expenses down to $24,000 per year. Therefore, he only needed $600,000 to retire by age 30. If you want more, here are four other examples.

While your numbers will likely be different (I know mine are), the equation still works out the same. Practice some moderation in your spending, and early retirement will be closer than you think. Here are some useful strategies for stretching your budget.

9- Challenge All Purchases

There was a time when I cringed at the word “frugal”. Mostly because I associated it with “no fun”.

But now frugal means something different to me. It means: Getting exactly what you want at the lowest price. Not holding off on making the purchase. Not skimping on quality. Buying exactly the thing I wanted for the absolute best price.

I consider it to almost be like a fun sport! How low can I get the price?

When my wife and I wanted a new SUV, we didn’t just go out and buy the first one we test drove. There was a fair amount of research that went into it before ever set foot at a dealership. But even then, we walked away from several who were not willing to be flexible on price or give us a fair trade-in for our old vehicle. But make no mistake – we eventually found the right sellers and ended up getting the SUV we wanted at a great price!

Start doing this with your major purchases, and you’ll see the difference. I’ve been pleasantly surprised by how little effort it takes to knock 10%, 20% or sometimes even 50% off the price I thought I was going to pay for something I wanted or needed. And all that does is keep more money in my pocket!

10- Ignore the Noise

I’m going to circle back to my first tip to invest in your financial education because when it come to your money, there’s going to be a TON of noise out there trying to distract you.

There will be people that tell you everything from you’re doing it all wrong to you’re missing out on a great investment opportunity!

It’s all nonsense. The number one rule to money is to stick to what you understand. If anyone comes along promising you something that either doesn’t make sense or simply sounds too good to be true, it probably is.

Make no mistake – this happens to both smart and uneducated people alike. How do you think someone like the infamous Bernie Madoff was able to swindle so many affluent millionaires of billions of dollars with his Ponzi Scheme? The problem is that people allowed themselves to make decisions based on greed rather than using common sense.

Again, don’t listen to the noise. Make your plan, keep it simple, and stick to it. As I usually say: No one should care more about your money than you.

Readers – What steps to retire early can you recommend? What habits or tricks have you found to be the most effective (or ineffective)? What helps keep you on the path to financial independence?

Featured image courtesy of MMD, taken on the beach of Los Cabos Mexico

These days, a better term for “retirement” might be “financial independence.” That is, retirement isn’t connected to a specific age, and it may entail continuing to work or volunteer. It’s all about doing what you want, when you want.

And anyone can do it. Financial independence, after all, is a simple concept: you need enough money to create income to support your lifestyle for the rest of your life. That points to the crux of retirement planning: How much you need to save depends entirely on how much you spend.

The power of compounding is something that few people (outside of folks who read financial blogs) know too little about. Compounding is incredibly important but your really have to have a lump sum already saved to take advantage – that or start saving 50% of your income to build a lump sum fast. The key is to get as much as possible as early as possible, then you can relax a bit after you have a tailwind.