If you’ve got dreams of retiring early by age 55 or sooner, then you’ll be very delighted to know: This is a goal that is definitely well within your reach!

Believe it or not, our ability to reach financial independence is something that is completely dependent upon our own decisions.

It doesn’t matter if you’re in your 30’s, 40’s, or any age. If you want to make working optional and retire by age 55, then you just have to be willing to stick to a strategy that will get you there.

Forget about the things you think are holding you back. In no place do we see this more than in one of the most popular money-excuses “I don’t make enough money to ever retire”.

You might think that the dream of financial freedom is something that is only reserved for the rich or those who make over $100,000 per year. But I can tell you that a lot of the same tricks work even if you make much less than that.

In fact, for this post, I’m going to base all my calculations on a income that’s half of that rate using a figure of $50,000. And honestly, that’s not a bad starting point considering that the current average income in the U.S. is only $59,039. (Don’t worry. The same lessons will work even if you’re making more or less than these numbers.)

So before we address the question of “how can I retire at age 55 or sooner?”, let’s get a better understanding of how your retirement savings rate and net income will play a major role in your strategy.

Disclaimer: Some of the links in this post to useful tools we recommend are affiliate partners. This is at no additional cost or risk to you. To learn more, check out our Privacy Policy.

Building Your Retire By 55 Plan

There are literally thousands of ways you can save for retirement successfully!

Since this is just one little blog post, we’ll need to lay down a few rules and assumptions that will help us to better build-up our strategy.

Assumption 1: We’re going to use pre-tax retirement savings to fund your retirement dreams.

I’m a BIG advocate of pre-tax retirement savings. Because the money you save comes out of your paycheck before you pay taxes on it, this allows you to save potentially thousands of dollars each year. For me, I’d rather (legally) take advantage of the opportunity to keep more money for myself than have to hand it over to the IRS.

For our example, we’ll mainly be using the U.S.-based retirement plan, a 401(k), as our primary savings tool.

Of course, there are other retirement savings tools we could use as well or even in addition:

Assumption 2: You’ll want to continue to enjoy whatever quality of life you’re currently enjoying right now.

That means that by age 55 (or whenever we’re able to retire), you’ll be making approximately the same net take-home pay. No more and certainly no less.

What do I mean by take-home pay?

As you can probably guess, if you make$50,000 per year, are you really living off of $50,000?

Of course not!

It’s less because you have to subtract away taxes and 401(k) contributions.

No problem. But before we can calculate this, we’ll need to first establish how much we’re saving for retirement.

Assumption 3: Saving for Retirement – The False Start of 10%

The old, sage retirement savings advice I often read and see in just about every generic financial publication out there is that you should be savings at least 10% of your income for retirement.

Simply to make a point, I’m going to use this 10% figure as our starting point.

(And then I’ll show you why this is NOT the savings rate you’ll want to use if you want to retire as soon as possible.)

Putting it all together – Our actual take-home pay:

Now we can actuate what your true net take-home pay is:

- Start with your gross income. In our example, we’ll assume you make $50,000 per year before taxes.

- Subtract your 401(k) contribution. As we said, we’ll assume you’re contributing 10% of our income to your 401(k) every year. That’s $50,000 x 10% = $5,000.

- Subtract Federal taxes. In the U.S., your annual Federal taxes are calculated by taking your gross income, subtracting away your 401(k) contribution and your standard deduction (as of 2018, personal exemptions are no longer applied). If we assume you’re married and filing jointly, this drops your taxable income down to $21,000. Using our marginal tax bracket system, that calculates out to $2,484 in Federal taxes for the year.

- Subtract away FICA (Social Security and Medicare) taxes. At rates 6.2% and 1.45% against your gross income, that’s $3,825 per year.

- State taxes. For simplicity, we’re going to ignore State taxes because there is a wide range of rates to consider. To keep the example light, let’s just assume this is one of your expenses you’ll cover with your net pay.

Putting all of that together, this means that you truly live on a net take-home pay of about $38,991 per year (or $3,249 per month).

What is Your Target Retirement Income?

So now we have a much more accurate picture of how much money we’re REALLY living off of in the present.

Good … but what does that mean for the future?

Again, we could go in many different directions for that question. But to keep this example simple and concise, one of the assumptions we’re going to make is that you’re going to want to continue to enjoy the same standard of living you’re already accustomed to.

In other words: Whatever your net take home is now will be what our target is in the future.

(Feel free to use whatever goal you want in your own calculation.)

There will be just two caveats:

1- Inflation:

The first thing you have to understand about the future is that inflation makes everything more expensive. Obviously you already know this because things you buy today probably cost you more than they did a few years ago.

Fortunately for you in this example, we’re going to be doing our calculations with inflation adjusted returns.

So no worries!

That means we’ll assume that $38,991 today has the same purchasing power it will whether we’re looking at 20, 30, or even 40 years from now.

2- Taxes:

If our net take-home pay is $38,991, is that all the money we’ll need in retirement?

Unfortunately, no.

Because we’re assuming this income will come from your pre-tax retirement savings, that means you’ll likely have to pay those taxes when you finally retire.

Therefore, you’re going to need a little extra dough to cover Federal taxes.

How much extra?

That’s a bit tough to answer since no one knows what the tax code will look like in 10, 20, or 30 years.

The best we can do is assume that whatever Federal taxes you’re paying now will be similar to what you will pay in the future.

If we go with that logic, then we can calculate our true retirement income needed as:

$38,991 + $2,184 = $41,175

What about FICA taxes?

Thankfully, you do NOT pay FICA (Social Security and Medicare) taxes on your retirement income. These were already paid on your gross income while you were working.

What is Our Target Nest Egg Size?

Okay. Now we have our target retirement income size.

From here, we can reasonably estimate the size of our target retirement nest egg by using our old-friend, the 4 Percent Rule.

Remember: The 4 Percent Rule says that says you should be able to safely and consistently withdraw a portion of your retirement savings equal to 4 percent of your starting nest egg balance year over year with inflation adjustments for the next 30 years; regardless of whatever happens in the markets.

Since our goal is to retire by age 55, that will take us to at least age 85 (and probably longer).

To calculate your target nest egg size, simply divide your target retirement income by 4 percent:

$41,175 / 0.04 = $1,029,375

How Many Years Will We Have to Save?

NOW is the part where we consider how long it will take to achieve our retirement goal.

In order to figure this out, you’ll need to consider 2 more very important factors:

- How much return you’ll make on your investments each year.

- Your annual savings rate.

Investment Return Rate

Again, we could talk for days about all the different types of investments there are and whether or not you’d ever want to invest in them.

But if you want my advice, the easiest way to approach investing is to simply put your money into a stock market index fund.

There is a TON of evidence to support why this is a good decision. In fact, there’s a whole forum called the Bogleheads devoted to the idea.

For our example, let’s say you take this approach. On average, the stock market makes a 10% return each year (when you look at it over the course of 10 years or more).

Remember that we said we’re going to adjust our example for inflation. Inflation is roughly 3% per year.

So to figure out the true rate of return on our investments every year, we subtract:

10.0% – 3.0% = 7.00%

Your Personal Savings Rate

As we’ll soon show, how much YOU plan to save each year will have a BIG impact on how quickly you retire by age 55 or before.

As we’ve already said, we’re going to start off this model assuming you’re saving at least 10% of your 401(k) each year. (And then I’ll show you why that won’t work …)

Raises

Can we assume we’ll save more each year because we might get a raise?

You could. But unfortunately I’d guess that most raises (if you get them) are about 3%. That means you’d be getting just enough of a bump to keep up with inflation.

So since our example is inflation adjusted, 3% – 3% = 0% increase in purchasing power every year. In other words, we’ll keep that $50,000 income the same throughout this example.

Employer Matching

Now the good news: In addition to your own personal savings rate, there’s one more thing we haven’t considered that will really help you out each year:

The 401(k) employer match!

401(k) employer matching plans are as far and wide as you can imagine. Some are very generous (matching dollar for dollar). Others give you nothing.

On average, we can find that most employers will match an amount that is equal to roughly 3% of your salary. So for simplicity, if we use this figure, this means you’ll be saving an additional:

$50,000 x 0.03 = $1,500

Combining your 401(k) employer match with your 10% savings, that’s:

$1,500 + $5,000 = $6,500

Putting It All Together

Combining a savings of $6,500 with a return rate of 7.0% per year, how long will it take us to accumulate our target nest egg of $1,029,375?

The answer: 37.3 years

… Hmmm …. Now you can see why a savings rate of 10% is NOT a good choice.

In order to make our age 55 target, you would have had to start saving your money around age 17.7. (… Weren’t you thinking about saving for retirement at age 17? …)

How Adjusting Your Savings Rate Will Lower Your Number of Years of Saving

As you can guess, to reduce the number of years of saving required, we’re going to have to bump up that savings rate.

And potentially by a lot!

But by how much?

Well, the answer will depend on you and what age you’re starting at.

If we were to run through this same model over and over again using multiple savings rates, we can get a very clear picture of just how much time we’ll need to achieve our goal.

Example

Say we’ve only got 20 years until we turn age 55.

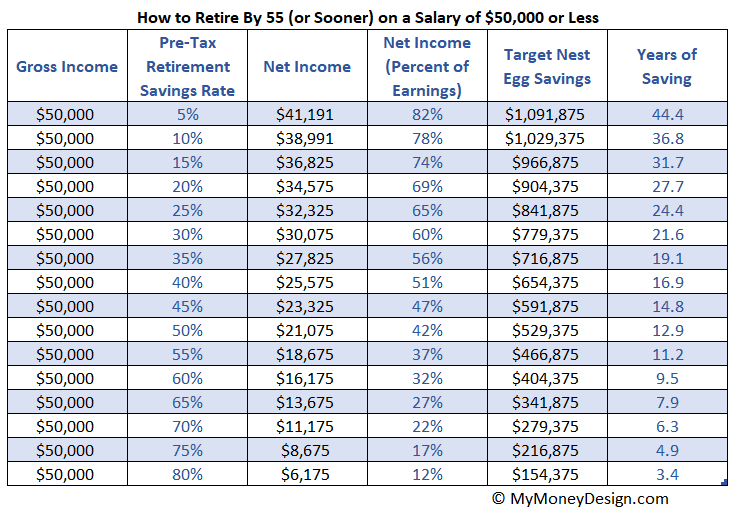

Using our chart above, we can see that we’ll need a savings rate of roughly 30-35% to accomplish this goal.

Can someone really retire with a nest egg of $500,000?

Absolutely! Check out my post How to Retire on $500,000 In Your 50’s or 60’s for all kinds of good tricks to make your dollars stretch.

Why Saving More Equals Needing Less

One of the most under-estimated aspects of financial freedom is just what an important role frugality plays.

Take a good look at the chart above … notice anything interesting?

In every row, you earn the same amount of gross income. But as our savings rate changes, your net income is reduced.

Is this a problem?

In reality, no. Since your income is spread out of the over the course of a year, you adapt. If you can stay disciplined and stick to a budget, then your lifestyle will adjust to fit this new level of income.

And then something beautiful happens …

Because you need less money to cover your expenses and live happily, that means you need to save up less money in your nest egg in order to retire. And that means fewer years until reaching financial freedom!

Example

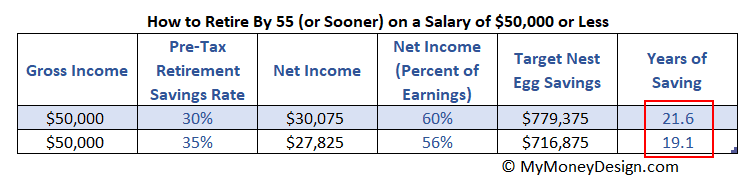

Take a look at the lines for 10% and 25% savings rates.

When you compare the net income you live off of at each of those rates, it’s a difference of $6,666 per year in the present.

If you can learn to live off of $32,325 instead of $38,991 per year, this shaves $187,500 off of your nest egg savings goal dropping it down from $1,029,375 to $841,875.

At that pace, you’ll reach financial freedom in 24.4 years instead of 36.8 years, a difference of approximately 12 years!

Doesn’t that seem worth it to give it a shot?

This phenomenon is something I’ve called the double-ended approach to early retirement. Not only are you saving more money to reach your goal faster, but you’re moving the goal-line closer to you by needing less money to get there. Though its very subtle, it can be a very useful strategy to reaching financial freedom without a lot of extra fuss.

What About Social Security?

Why haven’t we talked about Social Security here? After-all, if we’re using age 55 as our bench-mark for retirement, shouldn’t Social Security work into the equations (since you can most likely start collecting it at age 62)?

The answer is, of course, yes!

But Social Security is not such an easy topic to reduce down to just model. As you might already know, there are lots of different factors that can play into when and how much money you’ll actually receive when you’re finally eligible to receive Social Security. Some people might start collecting it right away and only receive hundreds of dollars per month whereas others might delay it and receive thousands.

If nothing else, we can think of Social Security as a buffer or safety net for using the 4 Percent Rule. As I’ve shown in this post here, when you factor in Social Security to your retirement plan, you can almost raise your safe withdrawal rate by approximately 0.5-0.75%.

Therefore, if you thought 4.0% was a bit too high for a safe withdrawal rate, we could assume that our Social Security income with help to supplement our income. This should give us more confidence that we will not run out of money.

Let’s Make Planning Easy!

If all of the math and variables seems overwhelming, don’t worry! I’ve got a solution.

There are lots of good online calculators that can help you shape your way to financial freedom. One that is particularly useful is the free Retirement Planner from Personal Capital![]() . It takes your desired retirement age and target income and then shows you how long your money will hypothetically last (best and worse case scenarios). From there, you can play and tweak these variables until your plan starts to look more like something you’d like to pursue.

. It takes your desired retirement age and target income and then shows you how long your money will hypothetically last (best and worse case scenarios). From there, you can play and tweak these variables until your plan starts to look more like something you’d like to pursue.

To use it, all you need to do is sign-up and then link your retirement accounts. Not only will this give you realistic numbers to feed into the Retirement Planner, but it will also provide you with a one stop-shop to see your nest egg all in one place and up-to-date each day. Very useful!

The Alternative to Saving More Money

Okay, okay …

So maybe hiking your savings rate up to 25% or higher is just something you don’t think you can do.

I get it … we’re all human.

The good news: There is an alternative strategy to saving your money.

What is it?

Earning a supplemental income through other means. This could be done either through an asset, side hustle, or part-time income.

How does supplemental income change my retirement goal?

Consider what would happen if you were to find a means where you could a reliable $500 per month from some other income source.

In the traditional system of retirement, you would have needed a nest egg of $500 x 12 x 25 = $150,000 to generate this income passively.

Increase that number up to $1,000 per month, and now you’ll need $300,000 of nest egg less.

Ways to generate supplemental income:

Like we already mentioned, there are a couple of ways to generate additional income outside of your retirement savings.

- Passive income streams. Know anyone who owns rental properties or receives checks from dividend stocks? There are tons of ways generate passive income streams that will help support you into retirement. Check out our extensive list here.

- Start a side-hustle. Side hustles are all the rage these days. And thanks to the Internet, they are easier than ever to get started. You could pick up freelance writing or become a virtual assistant. Even something as simple as collecting advertising revenue from running a blog can help generate a few hundred dollars per month.

- Get a part-time job. No one ever said that retirement has to mean “no more work ever”. Studies have shown that at least some level of work or activity in retirement can be just as good for your body and mind as it is for your wallet. Consider taking on a low stress job where you only need to work a few days per week with coworkers that you enjoy.

The takeaway in all of this:

The answer to “Can I Retire at 55” is possible. Financial freedom is possible. But getting there isn’t something that’s just going to happen. There are no shortcuts to early retirement planning. Though it can take a little thought, planning, and execution, it’s totally possible to devise a strategy that can and will work.

Readers – Do you believe it’s possible to retire early under an income of $50,000 or so? What do you think of this model? How would you help someone at this income level to retire by age 55 or sooner?

Photo credits: Chi King | Flickr /Brendan Riley | Flickr /Earl | Flickr / Mars Hill Church Seattle | Flickr / 21sacraments | Flickr

{kind=link}

If you get used to what you take home and not what you make, anyone can retire when they want. It’s easier with a higher income, but it’s possible for middle income earners as well. This also works for people who got a late start, like us. We’ve had to really ramp up savings and also added some rentals, but I should be able to retire around age 50-52. Very exciting!

Exactly. The more you can learn to live without now, the better off you’ll be in the future because you’ve already conditioned yourself to become accustomed to that level of income.

Yes, you can use this strategy at pretty much any point in the timeline – no matter how old you are or when you get started. But starting as early as possible makes it a lot easier to get those compounding returns put to work.

I’m 55 and planning to retire on the last day of 2019, at the latest 2020.. I’ve already began getting rid of the things that won’t be following me into retirement. Car payments….gone. Credit cards….never owned them. I have my military retirement and enough savings through my mutual fund, which I’ll draw from first, and my IRA, to hold me until I can collect my social security.

I’m nowhere near any of your nest egg numbers, but I’ve been calculating my figures for a couple years and am sure I can make it work for me.

Thanks for your added advise to what I’ve already been doing to prepare for early retirement.

I think it’s doable. The key for me was to pay off two mortgages. I’m working on paying 3 car loans and 2 credit cards within a year. I lately realize that debt and spending on unnecessary things just eats away any income.

We need a car, so I pay them off within 2 years and keep them for 10 to 15 years.

I know the less stuff I get now, the less I have to work and the more time I get to spend with the family.

My parents retired early on modest incomes. It can definitely be done. On the other hand, it becomes immeasurably easier if you earn more!

It’s only easier when you earn more if you can live like you have a modest income. Then, that way, you can bank the difference without any discomfort.

I think it can most definitely be done, as you’ve shown, but I think a good bit of it comes down to focusing on it as a goal. I know my Mom and step-dad were able to retire, and live relatively well in retirement, on pretty modest salaries. They created multiple streams of income and saved like crazy, so it can definitely be done.

Absolutely it has to be a goal! But a goal that can be achieved nonetheless. The great thing about focusing on your income is once you find one way to create a new stream, its only a matter of time before you start making more of them.

$50k in some states can get you a long way! So location definitely plays a role for sure. If you can keep your expenses down, it’s definitely doable. If you want to do it in some Northeastern cities or in California, good luck 🙂

Yes, in some states a literal income of $50,000 won’t work. $50,000 was just a number I choose for simplicity (and because it was so close the U.S. median household income). I’m sure the median income in California is probably a lot higher than it is around the country. So whatever that figure is, I’m sure you could plug it in to this formula and it would probably actually work.

Actually, you missed an important factor here — Social Security. Retiring at 55 might be easy even under the first scenario if you have enough to cover years 55-67, since at 67 (or even better 70, so as to maximize payouts), Social Security will start replacing some significant portion of your withdrawals from your nest egg to cover your income needs.

I know it’s all trendy to say “Social Security won’t be there for me” but that’s a highly dubious position to take for one of the most popular legislative programs in the country (and one that is relatively easy to “fix”….hell, even if nothing is done, Social Security can last pretty much indefinitely paying 70% of benefit levels). So not only does the 10% plus employer match get people pretty close, if you factor in Social Security they may end up having a better life/more income in retirement than they were used to having while working.

I always wonder what will be the final outcome of Social Security in the US. While it may not disappear entirely, what happens if the purchasing power of your Social Security income is vastly diminished by a financial crisis? Does me no good to receive $5,000 a month if that only buys me a loaf of bread. Or, given today’s news about the Grexit, what if China calls in their slice of our American pie and cancels Social Security as an austerity measure? We are in strange times, where cultures clash and consequences are kicked down the road. Until you run out of road…

Social Security may or may not be here when you reach older years. But regardless of what happens once you get there, I wouldn’t assume it will be there and be as helpful as you might want it to be.

If China decides to cash in their American debt one debt, you can basically forget about everything we just talked about in this blog post. There won’t be any retirement for ANYONE!

Well, for one, Social Security is indexed to inflation. If bread costs $5k in the future, you’ll be getting far more than $5k in Social Security benefits.

Second, why on earth would China ever call in its debt? Doing so has no business justification (we want our money back NOW, rather than collecting additional interest on it for the foreseeable future?), and would (a) wreck China’s largest market for goods and services, (b) risk default by the United States (in which case China gets nothing), (c.) destablize the global economy, and (d) potentially lead to war (very costly, very deadly, and one China would be likely to lose given US defense spending compared to China). Even if they did so, it wouldn’t mean a cut to Social Security (China doesn’t suddenly have legislative and executive power over the US to order ANYTHING as an austerity measure just because it calls in its debt). And how would it even do so? US debt is held by the Chinese government, but also millions of businessmen, entrepreneurs, companies, etc. in China — the logistics of even coordinating such a thing are mind boggling and strain credulity.

No offense, but you might as well be more terrified of alien attacks than of China somehow “calling in all its US debt.” Aliens from outer space are far more likely to wreck your retirement than China calling in its US debt.

Good point! I intentionally left Social Security out of this early retirement scenario because of the 7 years (ages 62 – 55) or more where you wouldn’t be able to depend on it. BUT if you factor it in at age 62, 67, or 70 (which ever you prefer), it does significantly impact how much money you’ll actually need to replace using your nest egg; thus lowering the overall amount you need to build up and save.

I also left Social Security out of the formula to spare the hail of comments saying “Ha! .. Social Security won’t even be around when I’m older.”

I’m actually one of the few personal finance bloggers I know who thinks that Social Security will be around in some shape or form by the time I’m ready to qualify. By their own admission, they will be able to pay 77 cents/dollar after 2033. That’s still NOT 0 cents! Even in that depleted state, that’s still going to be a couple of thousand or so for some people. I wouldn’t really dismiss it.

Plus 2033 is a long ways away. I’m sure that before then there will be some politician or political group that makes an issue out of this and does something about it. Either they will find new ways of funding it or simply change it into something else completely.

Can you imagine if they didn’t? All those millions of people who spent 30-40 paying into the Social Security system all this time and received nothing in return would be rioting in the street demanding blood!

Exactly. And the Social Security “fix” is VERY simple politically compared to other spending issues (Medicare, for instance) out there — some combination of (a) increasing workers paying into Social Security (say, with an immigration fix/increased legal immigration), (b) increasing the amount of income subject to Social Security taxes (right now you stop paying Social Security at around $110k or so in income….eliminate that cap and suddenly Warren Buffett and others are paying far more in Social Security), (c) reducing/capping cost of living adjustments (maybe not entirely doing so, but using a conservative inflation number), (d) eliminating Social Security claiming “strategies” that allow some couples to claim more, (e) increasing eligibility ages, (f) cracking down on Social Security Disability claims (to make sure they’re going only to the truly disabled, and not those who could work but choose not to), and (g) making cuts to other government discretionary spending (such as defense) and using the extra funds to shore up Social Security.

Politically, any one of these may be toxic to some constituency, but combined in some form they all could be palatable (and certainly would be versus cutting Social Security to 77% in 2033).

Those are all really good suggestions.

Do you think they will ever move towards the privatization of our benefits?

Oh, and this still ignores how rising middle class wages (perhaps spurred by initiatives to increase minimum wage nationwide and/or recent changes to overtime pay rules that could impact millions of workers) would likewise increase Social Security tax revenues…..

In short, there’s a lot of reasons why Social Security will, almost certainly, exist in the future in a form similar to today.

Nice analysis MMD! I’d agree that much of it comes down to expectations and what you intend to live on post-retirement. My parents had very modest lifestyles (and never made 5ok per year) and were able to retire early. But it had to do with wise lifestyle choices from age 30-50 that allowed them to do so.

I’m starting to notice a very positive trend with personal finance bloggers and parents who were able to retire early (mine included). Maybe this is why we are all so good with money? 🙂

My Dad retired at the age of 63 years. He said that he would have wanted to work further because he could still work and this could still boost his retirement fund. But, he was ready to retire by the age of 58 years. It’s worth it because he felt fulfilled and accomplished that he achieved more than what was expected. And, now he enjoys his retirement years!

Nothing wrong with waiting until you feel like the job is done! Good for him that he gets to enjoy his well-deserved time off.

I contended, in this post, that inflation can be largely ignored when calculated purchasing power in retirement.

The reason is because the breakdown and amount of expenses as you age tend to decrease. If you’re in your thirties or forties, then you’re probably spending the most money per month than you ever will. If you can control lifestyle inflation, then you’ll eventually have your house paid off, cars paid off, kids out of college, and you’ll live and travel smarter as you grow.

Each individual item will undoubtedly cost more, but the quantity of items you need as you age decreases dramatically.

A better way in determining your required nestegg is to instead look what expenses you’ll need in retirement to live your most happy life. Don’t start from any baseline. Start at zero and build up until you have a lifestyle that you love. For us, that turns out to be about $40k with housing costs, or $30k without housing. Forget that I make far more than that now.

Food for thought. Thanks for posting.

Eric

Interesting argument Eric … I’ll have to check your post out.

Normally every personal finance blogger in the world is ready to scream bloody-murder and fowl when you present a retirement plan when it doesn’t include some sort of inflation-indexing or compensation for future-value. You’re the first person I’ve ever heard of who has ever debated in the other direction! It never hurts to think outside of the box.

Good examples on the savings rate and the years till retirement, that struck a nerve. A 90% savings rate will have you in retirement in like 7 years or something crazy like that. Reaching it is hard, but def. doable for the average person who cares about the future and wants to be free.

You know, as ridiculous as a 90% savings rate sounds, I can totally see how it would be possible in some circumstances. Say you’re a young 23 year old professional who still lives at home with mom and dad. Many of my colleagues fit this bill when I first started working. If you’re really focused on early retirement, then there’s no reason a person in that situation couldn’t make it work in 10 years or less with an ultra aggressive savings rate. You just got to keep your expenses low and stick to it.

It is all about consistency. Just like anything, to be successful it takes a relentless pursuit. I have no doubt that if you are disciplined and diligent, anyone can achieve retirement success. Do the research and planning and then stick to the plan.

Well put!

I know people are nervous to count on Social Security, but the fact is that it will still exist when we retire. So while people should definitely make sure they’re secure on their own, SSA payments will help. My FIL had to retire early and he still gets over $1,100. Or about 1/3 what your target is.

Definitely. Social Security, whether its in one form or another, will exist in the future and pad the amount we need to save for our nest eggs. There’s no need for anyone to write it off from their retirement plan.

Haven’t been online for a few days. Came back to see this post and my shout out in the beginning. Holla!

And now after reading this, it looks like “early retirement” for me will be when I’m 75………………..Holla!

You are right about the conventional system being rigged, moreso nowadays than ever. I’d have to get a couple more promotions and increase my 401k savings rate just to be able to retire at 62 if I take the conventional route to retirement! Fortunately, I’m not planning to go the conventional route (I consider simply increasing your 401k contributions to be the conventional route).

Call me childish, but to me, 55 is not early retirement. 35-40 is early retirement. And even that’s a little too long to wait (a quick look at my blog would show anyone that waiting more than a couple years for retirement would require a level of endurance on my part that no human is capable of). And while saving is important, it can only get you so far (even contributing 6% to my 401k simply does not afford me enough per paycheck to live on and meet my financial goals, even after my recent promotion. Of course, I don’t make $50,000/year). At some point, you have to make more money, and not just from your job. Those passive income streams are what will make or break your early retirement strategy.

For me, my retirement vehicle is dividend growth investing. Rather than the traditional 4% safe withdrawal rate, the bulk of my investments are in income-generating blue chips with a history of rewarding shareholders with a growing share of the profits. And a small part of my overall portfolio is P2P lending, as you may have guessed from my recent guest post here. But mainly dividend investing, and ALL income producing assets. I’m not a fan of equity, capital gains, and other “paper wealth” forms of investing that require you to sell assets for money. How valuable was the asset if you had to get rid of it in order to see income (and only one single time), and what do you do when you need MORE money? How valuable is an asset that only makes a hallow promise to pay you in the future, or has a fluctuating value that only promises to pay you more money if you offload it RIGHT NOW (because it could bottom out a year from now). No, I’m only interested in assets that spit cash at me. If I have to get up and do something for my money, than I don’t like it.

But if dividend growth investing is my vehicle, then that vehicle needs fuel. And that vehicle is my current income. Dividend investing requires you to put in a lot of money and wait a number of years to get a good income, and so you need to make more money to invest. Right now I’m filling up using a cheap, low quality fuel called a paycheck. But I prefer high quality premium fuel–passive income rather than active income–fueling that dividend investing vehicle. And so I’m looking to build up my blog income–and start developing niche sites–that will supplement my paycheck funding my dividend portfolio.

With that, I’m also looking to combine that with something else: The backdoor Roth IRA conversion you spoke about! By turning my 401k over to a Traditional IRA and then slowly converting THAT into a Roth IRA (paying taxes as I go), I’ll be able to access my money before 59.5. That will make up for any shortcomings in my dividend growth investing. That information alone has made it possible for me to potentially retire a couple years earlier than I otherwise would have.

I’m glad you took me up on the “challenge” I made to you when I reviewed your book, MMD! Though I may have taken away a different message from the one you were trying to give us. For me, early retirement depends on one’s ability to build up streams of passive income and turn them into an income-generating machine. Simply increasing your 401k contributions, working more hours, and all the other conventional approaches won’t get you out of the rat race earlier than 55 years old (though that’s not to say that they are useless wastes of time; they can very much contribute to an early retirement strategy, but they can’t BE the strategy).

Thanks for the shout out and for taking up the challenge of outlining an early retirement strategy for those who aren’t making a ton of money.

Sincerely,

ARB–Angry Retail Banker

While I do strongly agree you need other income producing assets outside your job if you really want to accelerate your early retirement progress, I wouldn’t be so quick to write off increasing your 401k contributions as a viable strategy or even singular strategy.

You’ve got to remember: Everyone is just a little different in what works for them.

In other conversations I’ve had with people about how to retire early (age 55 or sooner), the very thought of starting a blog, writing an ebook, getting a rental home, or knowing which dividend stocks to invest in was as far-fetched of a task as asking them to fly to the moon. Those types of tools aren’t going to work for them. But when I asked them if they thought they could bump their 401k savings rate from 5 to 10 and perhaps 15%, it was something they felt was well within their grasp.

It all just depends on how bad you want financial freedom and what you feel you’re prepared to do.

No matter how you get there, I am glad to hear you’re doing something about your early retirement by trying to build up your blogging assets, P2P lending, and dividend income. I can totally identify with you in the joys of receiving dividend income – it’s really a great way to do absolutely nothing and make four figures per year!

Have you ever considered or looked into buying dividend stocks on a margin? I don’t use this strategy, but some of the more established dividend stock blogs I read in the past used to talk about it as a means of accelerating their portfolio growth.

Agreed, MMD, that some strategies just don’t work for some people. I can’t ever see myself investing in rental properties. That doesn’t mean that it’s a bad investment, but I can’t see myself going through the mortgage process (and I’m a banker!), or scouting properties, listing them, getting tenants, dealing with deadbeat tenants, suing someone or being sued, etc. Other people can do it, no stress, no problem.

But I think one has to look at what they want from their retirement and be realistic about taking a leap of faith. If “early retirement” to someone means retiring at 55 instead of 62, then fine, just raise those 401k contributions a little bit. To me, that’s like my employer offering me 50 cents more per hour and calling it a raise. Sure, it fits the textbook definition, but it’s not a raise.

Same here with early retirement. Retiring when I’m almost 60 isn’t early retirement. Retiring in my 30s is early retirement. And I’m sure many people who are reading this site are (rightly and justifiably) looking to escape the rat race now rather than later. I’m one of those people. But to make that goal a reality, increasing your annual savings can’t be your singular strategy (though it is a VERY IMPORTANT part of that strategy. It just can’t be the entirety of it). In your article about the conventional system being rigged, you calculated that even a whopping 50% savings rate would still require almost 20 years of 9-5 day job work to achieve retirement! 20 years!

Not only do I highly encourage those who wish to achieve early retirement to look at other methods of passive income, but I’ll even be the Debbie Downer and advise that if you are looking to truly retire early–earlier than even 55–than you HAVE to take that leap and do something that you can’t see yourself doing. You don’t have to become an oil baron or anything that really makes you uncomfortable. But you WILL have to do something, or you WILL have to accept decades of working for an employer. A year ago, I couldn’t have seen myself running a blog or anything to do with the Internet. I am NOT tech savvy in the slightest. But I took the leap (thanks, MMD, for talking me into doing it, by the way), and now I have a blog with actual visitors that sometimes make actual comments! Holy crap! Soon I’ll start making niche sites as well. Even if you’re not creative enough for that sort of thing, if you want to retire early, I really do feel that your savings rate simply isn’t enough. You have to do something to earn those extra passive income streams. Research. Start small with something that requires minimal financial or time investment, if you need. Do what’s right for you. But not doing anything because “Boy, that stock market is DANGEROUS” or “Wow, making money on the Internet is IMPOSSIBLE” or “I’m just not creative enough to write”, and then sitting around wondering why you’re stuck working until the age of 65? THAT’S the conventional method of saving for retirement, and that will get you nowhere.

That’s my two cents on it. Pretty much, if you’re looking to retire at 55, increasing your annual savings rate is all you need to accomplish that goal. If you’re looking to retire NOW (or within the next few years) as you write in your post about the conventional system being rigged, then you are going to have to get creative. For those with that goal in mind, I agree that the annual savings rate is an extremely important part of the strategy, but disagree that it can be your singular strategy. But you are right, achieving financial freedom depends on how badly you want it and what you’re prepared to do, and what works for one person may not work for another (like I said, you may someone out there who can invest in retirement properties no sweat, but can NEVER start a blog. That works fine).

As for buying dividends on a margin, I’ve honestly never touched options trading and probably never will. I’m not panning it, but I don’t really know too much about it and I don’t find it necessary to complicate my investing. I plan to hold onto high quality businesses forever. When I see value and I have the necessary capital and portfolio space (the latter being my biggest weakness), I buy. That’s it. Like I said, I’m not attacking options and margins. It works for other investors and I hope it continues to do so. But it’s not really for me.

Sincerely,

ARB–Angry Retail Banker

“………………..and I have the necessary capital and portfolio space (the latter being my biggest weakness)”

I meant the former is my being weakness. There’s always room in my portfolio for a high quality business that generates income. I don’t, however, always have the necessary capital to buy it.

Whoopsie.

This is really exciting news; I never thought it to be possible but it is great to learn that it is. This is definitely information that I will put to good use.

Thanks for this article, very instructive anf full of figures =) I think financial independence plays a huge part in retirement, it is obvious someone who’s been working for decades with 2 jobs will be able to retire sooner.

You’re welcome.

Great article! Thanks for breaking down all the figures. I’m going to try to apply some of these tips to my own savings.

Hopefully some of this will be useful!

Great post. This makes you think a lot about what goals you really have for financial freedom. We currently put away 15% for our retirement, but I don’t think bumping it up to 18% would make that much of a difference! In the long run it sure would.

Good read.

I think the vast majority of personal finance blogger are driven by this notion of early financial independence. I am no exception! The math I have done has lead to me to construct a Five Year Plan which would see me semi-retiring by the end of 2020.

I would have the option, of course, to work full-out for longer than 2020, but I’ll be 33 by that time and figure semi-retirement (working maybe 15 hours per week) would be an amazing position to be in.

All this because we pay attention to our finances. Great, eh?

Take care!

– Ryan from GRB

It’s amazing what kind of a difference you can make in your life when you pay attention to your finances and stick to a plan. I’ll have to read up on your 5 year plan. Being semi-retired by age 33 sounds very ambitious, but not out of the question!

Great article. I have been reading your articles for half years and like a lot of them. Keep up the good work.

Thank you very much! I’m glad to hear that.

Thank you so much for this article. Really informative without going into super-complicated investment strategies that no one but a financial guru would understand… it really gets me thinking positively 🙂

I have been gainfully working since I was 26 but immediately put all of my financial effort into paying off my student loans aggressively (sould be done by the end of the year!). I am 29 now and I have only been contributing the minimum employer match into my 401k (5%) and I have a fully vested amount of roughly $38,000 now. The catch is that I am not a particularly big fan of my job (where I am making $72,500) because it is highly stressful and I have come to the conclusion that I will look for other work once my loans are done. I was toying with how much of a pay cut I could take in order to have a gainful job but still maintain my happiness (strange priority; I know) and this article gives me a lot of hope. Currently I am throwing at least $2,000 of net pay towards my loans a month, and I have no desire to live anything remotely resembling an extravagant lifestyle so I’m now pretty confident that I could take a job at around $55,000 and feel very financially secure, especially knowing that I’ll pay off my mortgage by the time I am 60. Thanks again for the great, straightforward article.

You are very welcome Ann!

I can totally feel the pain of your situation. Balancing happiness and income is not always the easiest task. However, I do believe in the end that your mental well-being and stress level are worth every penny of however many thousands of dollars you have to give up in order to be where you want to be.

Since you mentioned taking a pay cut: Is it necessary that you have to go down? I only ask because I know a lot of people in my industry who have switched jobs, made higher salaries, and end up a lot happier because they finally found a better fit at a different company. Could that be the case?

Hi MMD,

As far as your question, not taking a pay cut would be awesome, but I have some other contingencies that would make finding a new job with equal or greater pay tricky.

Currently, I commute 60 miles round trip, and I want something much closer next, so I may have to be flexible with industry (maybe even “starting over” in a new industry, so to speak). I also want a first shift type schedule (in early, our early), and I’m not comfortable with being a manager, so I’d preferably like an hourly position. All of those things considered, I’ve come to the conclusion that I may need to face the reality of a pay cut to meet these requirements for what I want my work-life balance to look like.

Finance wise, I’m also exploring the option of eventually reverse-mortgaging my home after I pay it off to supplement my income in retirement. For what it’s worth, my boyfriend and I have the house together so we are splitting all home expenses.

I’m also aware that I will be able to claim social security in some capacity, but I don’t want to try to quantify it (and therefore, partially count on it) this early on.

Thanks for your question and let me know what you think 🙂

Wow, its funny how similar our situations are. I worked 60 minutes away from my home (each way) for 12 years. Finally I decided to switch jobs, and really had my heart set on finding something closer. But all the jobs near me pay about 60% of what I make now. So I ended up getting a different job … that is now 70 minutes away 🙂

BUT the job has way less stress and way less responsibility. So even though it pays about $10,000 less than my old job (and the drive still sucks), I’m very happy with it.

With that job change, I went from being a manager to being a worker bee again. Let me tell you – sometimes its awesome to not be so important.

Unfortunately, I’m afraid I haven’t looked to much into reverse mortgages to say if they are good or bad. I do know Dr Wade Pfau, a very respected and very technical figure in the retirement planning community, has written a number of articles on them:

https://retirementresearcher.com/what-is-a-reverse-mortgage/

https://retirementresearcher.com/using-reverse-mortgages-responsible-retirement-income-plan/

https://retirementresearcher.com/calculating-reverse-mortgages/

Thanks for the links; I will definitely check them out!

And yes, in a world that seems to be pushing worth in the workplace to run parallel with the “necessity” to achieve a management position, it good to know that others have found happiness in the exact opposite of that 😉

The extremely interesting article, thanks! In fact, I try to do smth like that now and can say that it really works.

I agree with you; it can be done as long as you live within your means. Having a huge income doesn’t mean you can retire early, and those with middle income can’t do it. Because it is also about people’s spending habits. Being frugal can do wonders for your future and so is taking time to make a plan, just like this one that you did. Taking to plan will help one know how much to save for retirement, that will enable him to do necessary action to meet that goal. Early retirement is possible but it requires effort and lifestyle changes.

Great article, I will definitely be using these tips.

Maybe it was already mentioned in the comments but… I’m curious what people are doing for health insurance when they retire so young being that it will be several years till they can collect Medicare.

Some really great advice here. It should be possible on an average income through frugality and investing wisely but very few manage to do it. I agree about putting money into index funds – you generally come out on top over picking stocks and it offers a well diversified investment vehicle.

Well…I enjoyed the article, so thanks for being thorough. I have heard that my Social Security is in fact going to be taxed…so maybe you can look into weather…as you say, it isn’t. That would be a nasty surprise for folks if it really is!?!?

You’re referring to this section?

“Thankfully, you do NOT pay FICA (Social Security and Medicare) taxes on your retirement income. These were already paid on your gross income while you were working.”

Please let me clarify: If you receive Social Security income, yes, you will pay Federal and State taxes on it, but you will not pay FICA. Here’s another article to help clarify: https://finance.zacks.com/pay-fica-retirement-income-1214.html