It’s my annual update to our plan for financial freedom.

Trust me – you’re not going to find another plan like this anywhere else.

For some time now I’ve been saying that my wife and I plan to retire when I turn 45 years old.

How do we plan to pull off such an ambitious goal? That’s what this plan is all about.

We put numbers to paper and actually see what our cash flow will look like all throughout the future. Hence the name of the blog, this is our “money design”.

If you have any desire whatsoever to retire at 45 (or any age really), but you’re not really sure how you’re going to do it, then this post is for you! I’ll show you exactly how we’re going to reach financial freedom, and how you can use the same strategies to get there too.

So without any further ado, let’s see how the plan is looking this year.

First – A Little Background:

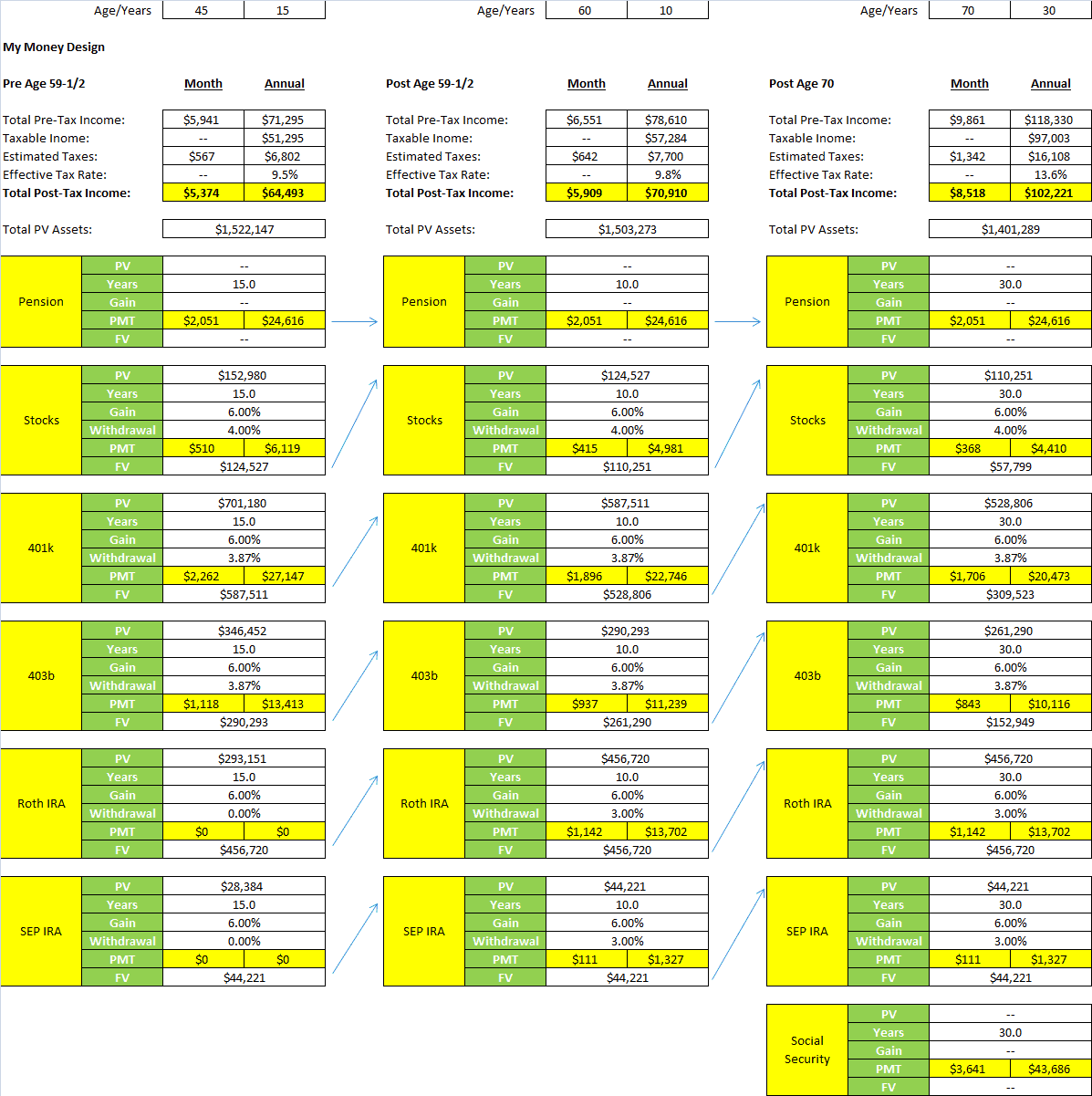

For those of you who are seeing this plan for the first time, here’s a little background on how the plan is structured. Basically our assets are arranged into three major groups (columns) based on when you can actually access them without penalty.

- Income from age 45 to age 60 (before we can officially access our 401k and IRA without penalty)

- Income after age 60 (after we can officially access our 401k and IRA’s without penalty)

- Income after age 70 (when we’re eligible for full Social Security)

Starting with the first column, the goal will be to withdraw a minimum of $5,000 (my pre-determined monthly retirement income) without depleting my resources for the second column.

The same is true of the second and third columns. Again the goal is to be able to withdraw my minimum amount needed without emptying all the accounts or sacrificing any other stage of my life to do so.

As long as all 3 columns support my minimum amount of income needed and don’t deplete, the plan is a success!

A few technical notes:

- Yes, this plan is inflation adjusted (assumes 3% every year)

- I’m assuming annualized investment returns of 6%

- Federal income taxes are calculated by subtracting a standard deduction and 2 exemptions (my wife and I) and using today’s standard marginal tax bracket system.

Our Plan to Retire at 45:

Here is the master spreadsheet containing all my calculations and estimations (click on the image to make it larger):

So Are We On Track to Retire at 45?

The answer is YES! By exceeding this income value in all three columns, I feel very comfortable in knowing that we’ll have a very comfortable retirement without fear of running out of money. (More on that to follow).

How This Plan Will Actually Work:

On the surface I realize there’s a whole lot of numbers, and the story behind what’s actually happening is probably getting somewhat lost. Here is a little bit more explanation as to what’s really going on behind the scenes.

From LEFT to RIGHT:

- Save a whole lot of money (don’t worry … we’ll get more into detail on this in the next section). Monitor their progress easily using free software like this one here.

- At age 45 is when my wife will become eligible to start receiving her full pension. At the same time we’ll take our 401k and 403b, convert them into a rollover IRA, and use a 72t to start taking out SEPP’s. (The numbers used in the plan were calculated using a 72t calculator.) Combine all that with our stocks and that will be our monthly income from age 45 – 60.

- After age 60 we’ll add in income from our Roth IRA and SEP IRA to boost our income up even higher. Technically we could start withdrawing more from the 401k and 403b, but there’s really no reason to change the low withdrawal rates quite yet.

- After age 70 both my wife and I will qualify for full Social Security benefits. The benefits used here were calculated using Social Security’s website and reduced by 25% to compensate for Social Security’s notice that they’ll only be able to fund about 75% of $1 after 2033. Regardless, now our monthly income will really be kicked into full swing.

- By keeping the withdrawal rates low from age 70 on, we should statistically never run out of money.

Things We’ll Need to Do to Pull This Off Plan for Financial Freedom:

In real life there are LOTS of things that will need to happen to make sure it is a success. Here are the main highlights:

My Wife’s pension. One key factor to pulling this whole thing off will be making sure my wife receives her full pension benefits. Basically she needs a minimum of 25 years of service (really its 30 but we bought 5 years ahead of time). Once she does that she’ll be eligible to start receiving guaranteed paid benefits every year. Another nice bonus will be that we will be able to latch on to her health care benefits for a decent price.

Save big! Normally when you retire at 65 you’ve got a ton of years to let compound interest work its magic and build up your fortune. That’s not necessarily the case when your plan is to finish working by age 45. Therefore in order to pull this off, we’ll need to:

- Max out our 401k plan – Accomplished!

- Max out our Roth IRA’s – Accomplished!

- Contribute as much as $500 per paycheck to our 403b. Right now that’s the savings rate we’re currently at. However I would like to see this go up.

Utilize tax efficient resources. Not only are we going to save our money in IRA’s and 401k’s, but I also plan to save as much of our blogging income as possible in a SEP IRA (find out how you can do the same in this post here).

Build up as many passive income streams as possible. Even with saving at the maximum contribution levels with my 401k, 403b, and Roth IRA’s, that’s not enough! To really make this happen we’re going to focus on building up the money we make outside our jobs – in particular my online business efforts. This year has been particularly great for us in this area. Just read by through any of our niche site income reports and you’ll see that we’ve been consistently making about $1,000 for the last few months.

Take advantage of lower capital gains and dividends taxes. As you might already know, capital gains and dividends are taxed at lower rates than normal earned income (15% vs 25%). By saving a portion of our money in these types of accounts we’ll not only keep the money more liquid but also be strategically them less expensive when it comes to taxes.

What Assurances Do I Have That This Retirement Plan Will Work?

As with many engineering designs, there are various safety factors built in to help ensure the designer that their creation will work. Here are mine:

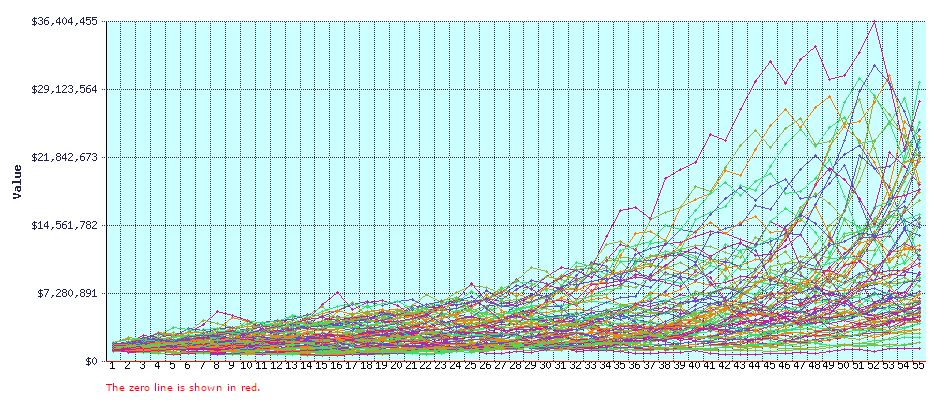

- It’s FIRECALC tested.

Do you ever use FireCalc? It’s a pretty cool free retirement analysis tool where you check to see if your money will last as long as you think it will. The way it works is it uses the past +100 years of market returns and shows you how your portfolio would have worked out for any time segment throughout history. By looking at the trends and seeing how many of them were successful you get a sense for how durable your portfolio will be (assuming history repeats itself).

So let’s play this game. If we assume I retire at 45 and I’ll live to be 100 (yes, we’re overshooting a bit here) then I’ll need my portfolio to last 55 years. Using Firecalc with an estimated balance of $1.5 million and a withdrawal of $48,000 ($4,000 per month not coming from the pension), then here are the results.

WOW! According to FIRECalc I will have a 100% chance of success with a possible average ending portfolio balance of $11,179,704. (Long live the MMD heirs!)

If I was willing to take on a little bit more risk and drop my chances of success back to a 95% confidence level, running the numbers again I find that I could withdraw as much as $55,000 per year (or $4,583 per month). Either way – it looks like we’ll be doing good here.

- I’m overshooting my basic needs. In previous posts we’ve already proven that $5,000 should more than cover our expenses throughout each stage of this plan.

- We’re inflation adjusted. By subtracting away inflation, you’re seeing all the numbers in today’s dollars which means we shouldn’t lose purchasing power.

- I’m using very conservative growth figures. Most of the time when people forecast market growth they assume a historical 9% growth rate (because that’s what an index fund classically returns on average). But with only 11 years left to go, what if stocks DON’T return 9%? What if it’s less? What if I intentionally invest more conservatively into a hybrid fund containing both stocks and bonds? What if I just want a safety factor? For all those reasons I’m using 6% as my growth value.

- My withdraws will also be very conservative. The popular 4% safe withdraw rate was only ever guaranteed for a 95% success rate for up to 30 years. By using figures closer to 3% instead of 4% within this plan we will almost guarantee success.

- This plan is tax efficient. Notice in the pre-age 59-1/2 days I’ll be relying on dividends for a decent chunk of the income. That fact combined with a modest income will help to keep my effective tax rate will be very, very low.

- I’m not considering or counting on future employer contributions. Because my employer’s contributions are somewhat unpredictable, I’ve decided not to include them in my future projections. They’re pretty much just icing on the cake. That not only helps to keep my plan more conservative but also helps to buffer any unforeseen dips in my balances.

- I plan to keep working and bringing in an income. On my own terms of course. As we’ve discussed before, I’ve given a lot of reflection as to what I actually want to do when I retire early and will do with my newly earned time. I’m pretty sure at least one of those things will be doing what I’m doing now … side hustles that generate cash!

That’s all I’ve got to say about this year’s update of the financial freedom plan. What do you think? Will I actually be able to retire by 45? Perhaps sooner? Is there anything in this plan that you didn’t know about already or that you think you might borrow for you own retirement plans?

Photo credits: Flickr, FreeDigitalPhotos.net

You and your wife should be congratulated for the great plan you have for your finance planning. I am being challenged to start investing and saving plans as to reach my financial freedom at the age of 45.

How many more years do you have to work with until you reach that age?

MMD, I am really impressed with your retirement plan! With that as specific, you cannot go wrong and are surely on your way to retiring at 45 or even earlier. By the way, I am inspired so I am planning to look for more side hustles and to increase my savings for my retirement plan next year. Congrats MMD! Happy Holidays!

Thanks Jayson. You’re looking in the right place if you’re thinking of adding some side hustles. Aside from using some common sense investing, making money on the side has been one of the biggest helpers in accelerating our wealth creation.

Sounds reasonable to me! In the worst case scenario, you could always readjust and add a few more years of work at the end- or lower your monthly spending to make it work.

I also think we can retire at around 45-46 BUT I doubt we will. We will have two kids heading to college around that time and I don’t want to quit working until I know their college costs are squared away. I bet we will fully retire around 50, but maybe partially retire about 46-47. We are 35 now.

We’ll be in approximately the same boat as far as kids in college. We’ve got 529 plans setup for them so we should be off to a good start as far as paying for college (for at least the first few years).

Love the detail MMD and think it’s definitely doable for you. Like Holly said, the worst case scenario you should be able to make some tweaks to it in order to work.

Right now, I’d say we’re likely on target for the ability to retire around 50 though a huge part of that depends on our business. Our kids won’t be hitting college until my mid-50’s either and we’d like to have a good bit put away for them so it would likely be put off until then. But, that said, a huge part of that goes back to the growth of our business.

I’m actually hoping that after we retire we’ll get serious about doing more with this online business (assuming it will still be around in 10 years).

Congrats to you and your wife! It’s awesome to see your hard work pay off. It’s also nice to see someone with such a solid early retirement plan who isn’t into the super extreme frugality. I love how your plan allows you to live a comfortable lifestyle during retirement!

NOT being ultra frugal was a key element. I’m glad you picked up on that. I didn’t want to jump on the early retirement bandwagon and pretend that we would be fine living off of $2k per month. I already know that that’s just not realistic for us. It’s important for people to set practical expectations and then work towards them so that they can live the life they want to; not try to box themselves into something they will regret later.

MMD,

This is a well thought out conservative plan. Looks like you have it nailed. I wish I could live on $5,000 a month, but SoCal is too expensive to pull that off. One thing you may want to think about for your third column is an estimate for an assisted living facility. None of us like to think about that, but the day will come for all of us when we can’t take care of our own home or ourselves. It is expensive and will only get pricier in the future.

Thanks,

Deets

Thanks! I was going for something as conservative as possible to help ensure success. Previous versions of this plan did not use quite such low numbers, and honestly it left me feeling uneasy.

Great point about the assisted living expenses. My grandmother was in a home for the last few years of her life and I remember my parents struggling to figure out how to balance her finances so that she could get the assistance she needed. Although I didn’t really bring this up in my plan, I had a hint of this in mind as I was setting things up – which is why the third column is so much higher than the others. I know that by the time I’m in my 70’s health will be issue and I wanted to make sure we had as much money as possible to combat it.

This is a very impressive plan. I’m single, myself, so I plan to keep my needs small. My present “can quit” date is 2025, though, like you, I plan to work at something else after I leave my career.

It’s my belief that what you decide to do after retirement is just as important of an element in your financial freedom plan as the path you take to get there. That single idea can be your guiding light and motivation when things get especially challenging.

Wow!! This is awesome and so encouraging!! We want my husband to be able to retire at age 45, too (12 years away), but we don’t have an exact plan yet. This is very inspiring to create one and I’m showing this to my husband tonight. Thanks!!

Thanks! I hope you both find tons of gold in this retirement plan that you can use for your own financial ambitions.

Great detailed planned MMD. A 100% success rate, and 11 million dollars sounds like a successful plan. Good Luck in 2015. I hope to be retired by 45-50 as well, but with much less money and income. Shooting for a 3 grand a month retirement income, with a 20% buffer to invest more into future investments, as to protect myself for inflation. Hope that made sense. With no debt, and my ability to grow any side hustle income later on, I feel that is enough for my lifestyle.

I’ve read many forums and posts where $3K per month is completely adequate. It’s all a personal decision.

I’d love to see you put together a plan that we can read about later on. I’m also interested to see how the side hustle income will play into that.

I love your plan. We’ve run FIREcalc several times. And have thought over and over, and over again, about what we need to do in order to reach our early retirement. But seeing your details has motivated me to create my own estimate of where our money will come from during that early retirement. I’m so glad I did it – seeing real numbers from real accounts makes the prospect of early retirement seem so much more within reach. Happy new year!

I’m really glad you got so much from this. You totally got what I was trying to do here – use real numbers and estimations to see exactly where we’ll be in the future. I also found that to be a far more powerful motivator.

Good to see you have such a detailed financial plan all laid out. I have to do something like that as well. I’m aiming to retire early, but with no real plan in mind other than “saving and making passive income”. That’s no bueno.

I also do like, as you mentioned in an earlier comment, that you aren’t jumping on the extreme frugality bandwagon. I love a lot of the blogs that have them, but I prefer to focus on maximizing my income rather than never spending money again. It’s also nice to see that it can be done without living off of peanut butter sandwiches forever.

I’m glad you picked up on that. I’m just not big on frugality. I think there’s a place for saving money and living modestly. But I know myself enough to know that $2K per month or whatever the minimalists shoot for is just simply not going to work. What’s even more encouraging is that if you study the way the wealthy live, they don’t settle for Ramen Noodles for dinner every night either. They plan, save, and invest to achieve they life they want to have rather than just scratching the surface.

This is awesome. It’s great to see such a seemingly ambitious plan broken down in plain English and understand how it can work perfectly.

Very impressive. I am just in my 20s and I commend those people who have brighter future like you and who believe they can. I want to retire at 45 also. I wanna be like you! Thanks for giving me inspiration and ideas.

Wow. What a great plan! You and you’re wife surely did a great job on planning all of these.

Amazing effort mate! Great to know that you’re on track.

I’m also shooting for early retirement, but I’m looking to exit work at 55yo, in the hope that I don’t need to draw down any of my pricinple investment, meaning Ikonz Jr is going to be the recipient of a VERY nice inheritance!

I love the Monaco simulation. Might have to do one myself on Firecalc.

Why withdraw so much from 401K/403B before age 60? you have a roth sitting there and all of your contributions are not taxable if you withdraw those… You can also transfer the roth max from 401K to roth each year and “season” those funds for 5 years and withdraw those without penalty as well (you’d have to pay regular incom taxes the year you transfer). This will allow your tax deferred $ to continue to grow unhindered by early withdrawals. Now you can retire at 44 (probably earlier as your plan is ridiculously foolproof and secure, congratulations!)

Hi Jake, welcome to the site!

Thanks for the recommendations It’s funny you bring that up just now. I’ll actually be posting a new update to this plan at the end of December. And yes, I will be making use of the backdoor Roth conversion ladder as well as a few other good tricks!

Do you have early retirement plans of your own?

I never thought about buying more of our pension. How did you do the math to see if the investment was worth it? Is your pension indexed to inflation? If not how are you compensating? We haven’t figured that out yet. We have a Texas teacher pension. Thanks!

An easy way is to look at the benefit and then multiply in by 25. For example, if buying extra pension will ultimately net you an extra $1000 per month (inflation adjusted) in the future, then that would be like saving an extra $1000 x 12 x 25 = $300,000. (This is the inverse of using the 4 Percent Rule for retirement.)

Next look at what it costs. If you couldn’t reach / invest your way to the benefit amount ($300K in my example), then its a good trade!

Obviously, also consider the stability of the pension provider. If they have a good history and there’s no bad news or press about the pension being underfunded or threats that it will be taken away, then this is also good news.